Under Ind AS, goodwill is no longer amortised. Instead, every year, companies like Tata Steel, Infosys, Wipro and ITC must check whether their goodwill is still worth the amount shown on their books. This is called the Impairment Test under Ind AS 36.

1. Why Impairment Testing?

- Goodwill has indefinite life — without an annual review, it could become overstated.

- Protects investors from inflated assets and overstated profits.

- Aligns Indian financials with IFRS (IAS 36).

2. Key Definitions

(a) Cash-Generating Unit (CGU)

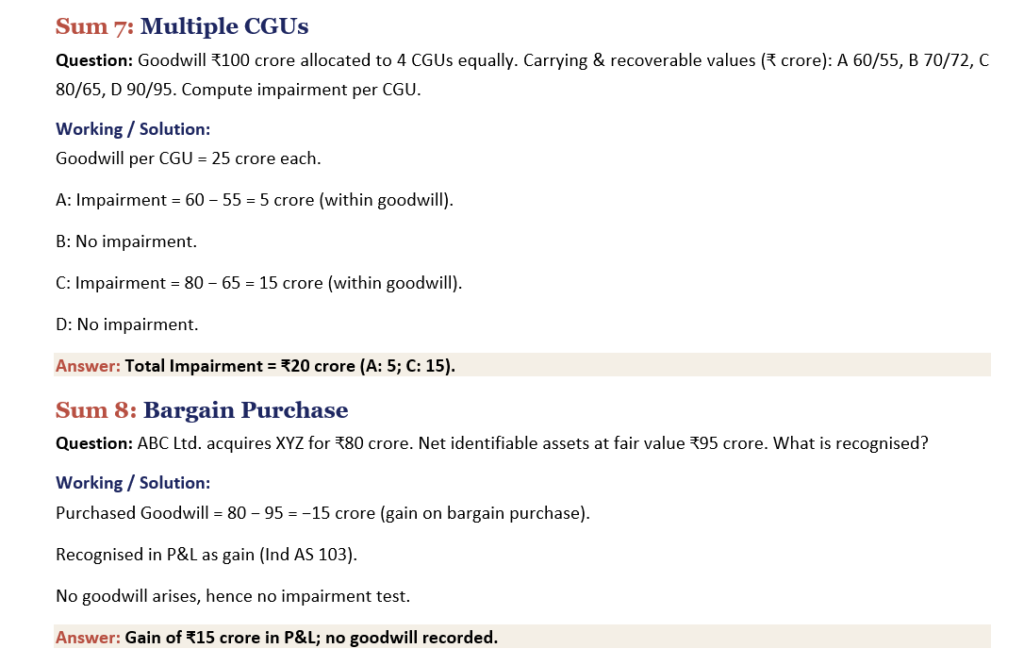

The smallest identifiable group of assets that generates cash inflows largely independent of other assets. Example: each business segment of Tata Group — Tata Steel, Tata Motors PV, Tata Motors CV — can be a separate CGU.

(b) Carrying Amount

Value at which the CGU (including allocated goodwill) is shown in the Balance Sheet.

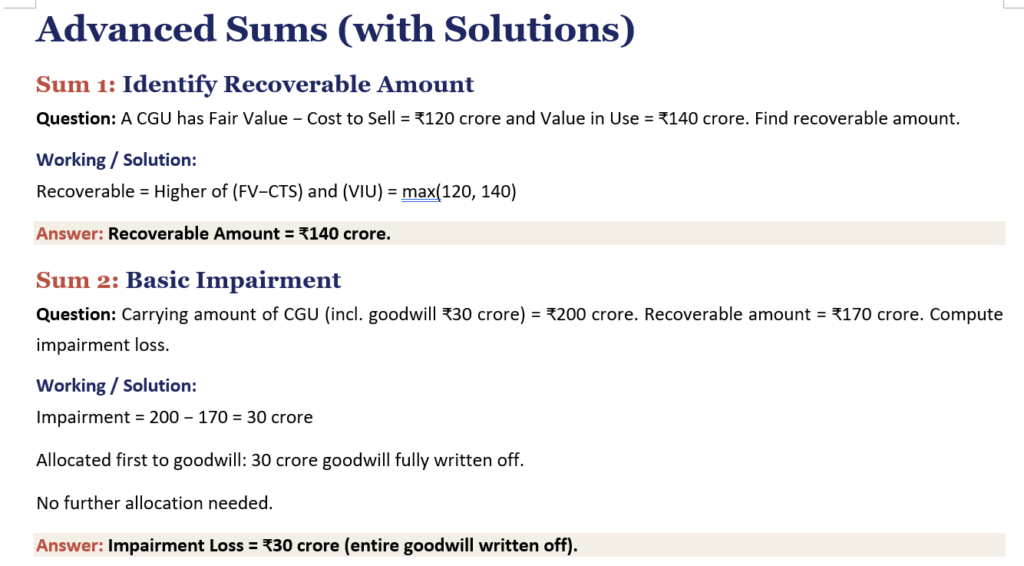

(c) Recoverable Amount

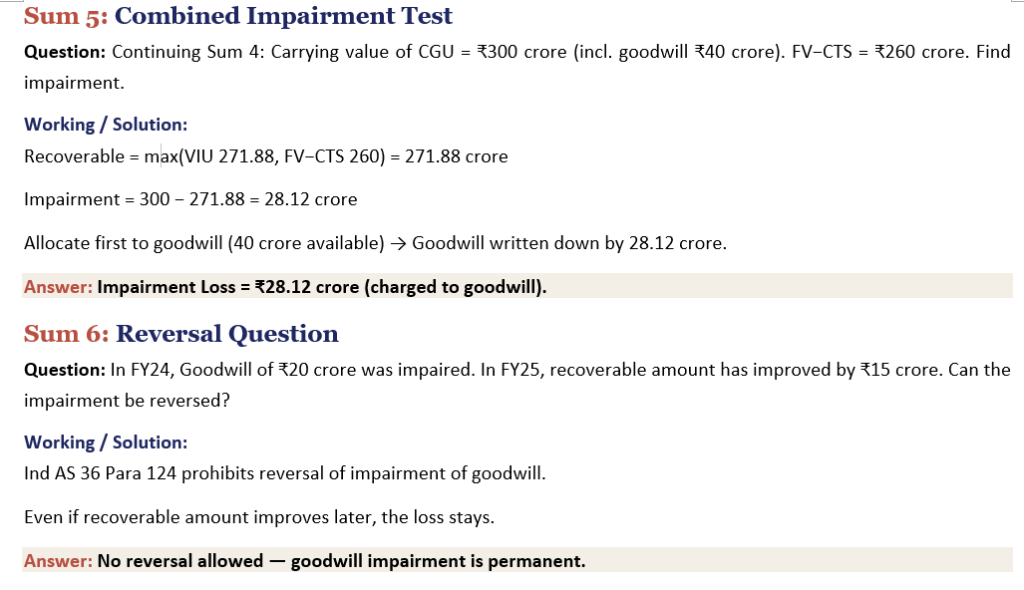

Recoverable Amount = HIGHER of (Fair Value − Cost to Sell) and (Value in Use)

(d) Value in Use

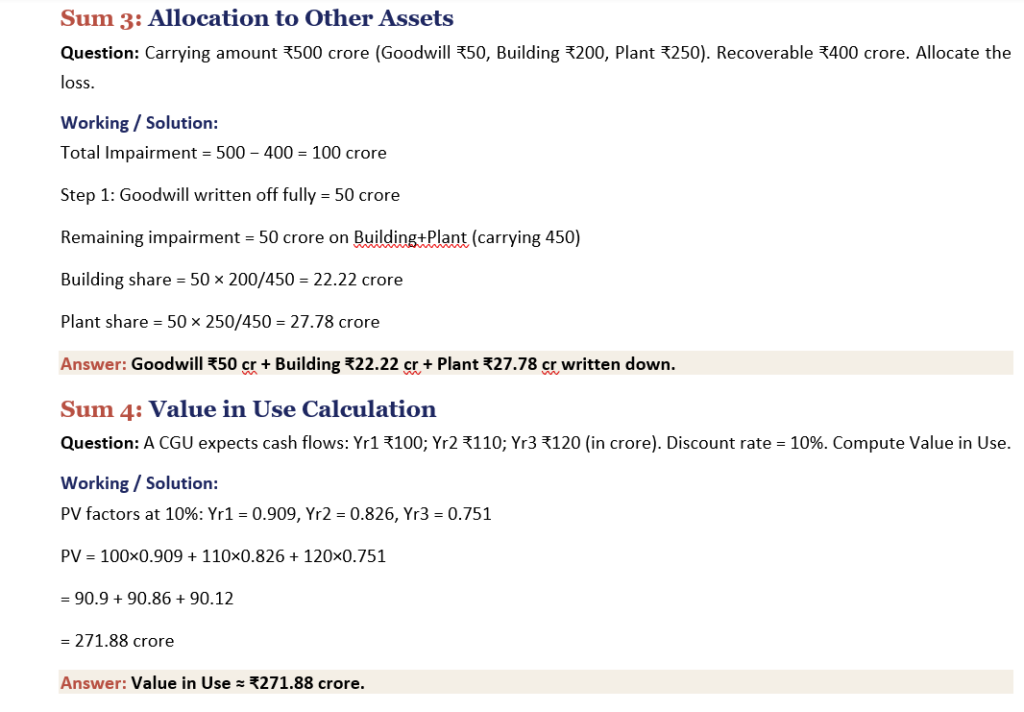

Present value of future cash flows expected from the CGU, discounted at a pre-tax discount rate (typically WACC).

3. The 5-Step Impairment Process

- Identify CGUs and allocate goodwill to them.

- Determine carrying amount of each CGU (including goodwill).

- Estimate recoverable amount.

- Compare carrying with recoverable amount; if carrying > recoverable → impairment.

- Allocate the loss: first to goodwill, then to other assets pro rata.

4. When Is the Test Done?

- At least annually, regardless of indicators.

- Whenever indicators of impairment exist (e.g., regulatory changes, technology shift, fall in market cap).

5. Reversal Rule

Important: An impairment loss recognised on goodwill shall NEVER be reversed in subsequent periods (Ind AS 36, Para 124).

6. Real Indian Examples

- Tata Steel impaired goodwill on its European business by thousands of crores due to Brexit and steel price collapse.

- Vedanta has tested goodwill on its Cairn India and copper businesses multiple times.

- Infosys and TCS routinely disclose CGU-wise goodwill and discount rates used.

7. Disclosures Required (Ind AS 36)

- Carrying amount of goodwill allocated to each CGU.

- Basis used to determine recoverable amount.

- Key assumptions and discount rate.

- Sensitivity analysis if a reasonably possible change would cause impairment.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.