Foundation note of Issue of Shares — meaning, purpose, types and share-capital terminology under the Indian Companies Act, 2013.

What is a share?

A share is the smallest unit into which the total share capital of a company is divided. Each share represents a fractional ownership interest in the company. Section 2(84) of the Companies Act, 2013 defines a share as a share in the share capital of a company and includes stock.

Example: If Reliance Tech Ltd. has share capital of ₹10,00,000 divided into 1,00,000 shares of ₹10 each, then each share is one out of one lakh equal portions of ownership.

Why do companies issue shares?

- Raise long-term capital for setting up factories, R&D and expansion.

- Spread ownership and risk across many investors instead of relying on a single promoter or lender.

- Avoid fixed interest burden — unlike loans, dividend on equity is paid only when there are profits.

- Improve credibility — a listed, broadly-held company commands trust with banks and customers.

- Acquire businesses or assets by issuing shares as consideration (covered in Article 6).

Types of Shares

Equity Shares (Sec. 43)

- Carry voting rights at general meetings.

- Dividend is not fixed — depends on profits and Board recommendation.

- Rank last for repayment in winding-up.

- Permanent capital — not redeemable (except buy-back u/s 68).

Preference Shares

- Preferential right to a fixed dividend before equity.

- Preferential right to repayment of capital on winding-up.

- Limited voting rights.

- Sub-types: Cumulative / Non-cumulative, Participating / Non-participating, Convertible / Non-convertible, Redeemable (must be redeemed within 20 years).

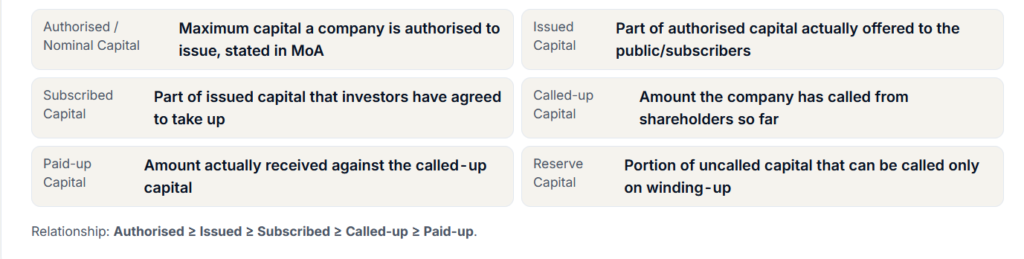

Share Capital Terminology

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.