Face value, Securities Premium Reserve under Sec. 52, and the legality of issuing shares at a discount under Sec. 53 / Sec. 54.

What is Face Value / Par?

The face value (or nominal value / par value) is the value printed on the share certificate and stated in the Memorandum of Association. Common Indian face values are ₹1, ₹2, ₹5 and ₹10. The face value is the basis on which dividend is declared (e.g., 12% dividend on a ₹10 share = ₹1.20 per share).

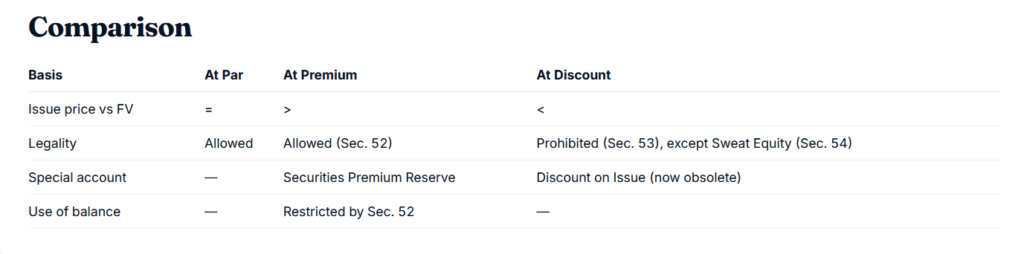

Issue at Par

A share is said to be issued at par when its issue price = face value. For a ₹10 share, the company collects exactly ₹10 from the shareholder (in one or more installments).

Issue at Premium (Sec. 52)

When issue price > face value, the excess is called Securities Premium and is credited to a separate account — Securities Premium Reserve. Section 52 restricts its use to:

- Issue of fully paid bonus shares.

- Writing off preliminary expenses.

- Writing off discount/expenses on issue of shares or debentures.

- Providing premium on redemption of preference shares or debentures.

- Buy-back of own shares u/s 68.

Premium can be called at application, allotment or any specific call — most commonly at allotment.

Issue at Discount — Rules

Section 53 of the Companies Act, 2013 prohibits issue of shares at a discount. Any such issue is void. The only exception is Section 54 which permits issue of Sweat Equity Shares at a discount to directors / employees, subject to conditions.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.