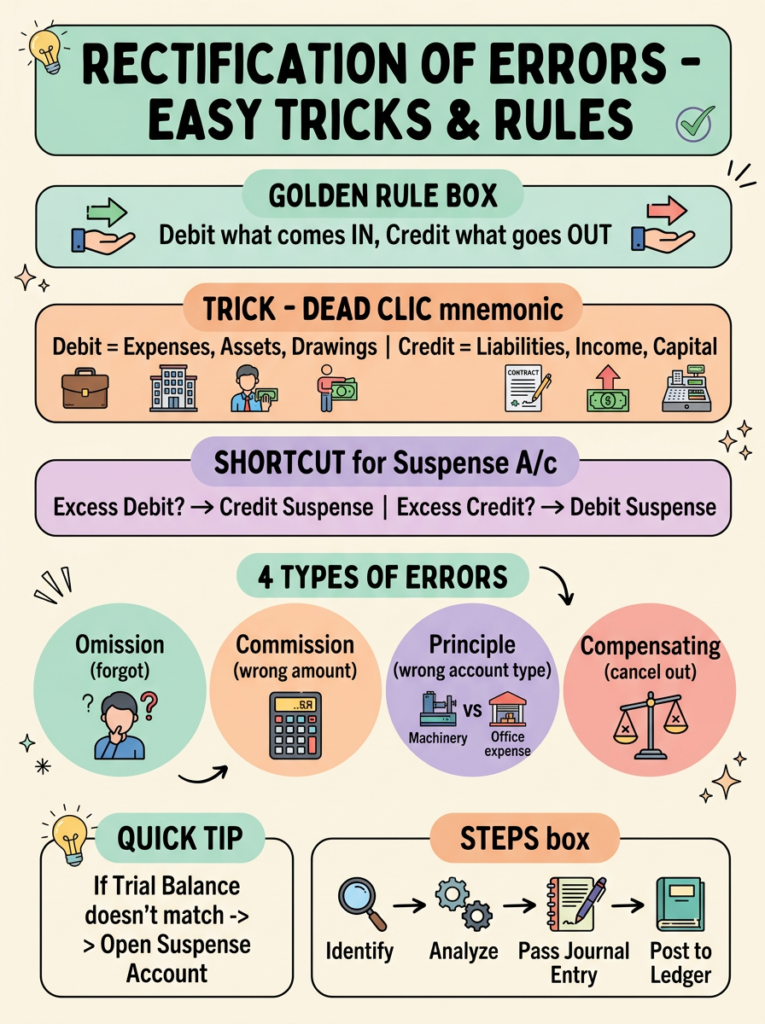

1. What is Rectification of Errors

Rectification of Errors means correcting the mistakes that occur while recording, posting, or balancing accounting transactions. The objective is to make the books of accounts show the true and fair financial position of the business.

In the real world, no accountant is perfect — small mistakes happen during journalising, posting to ledgers, casting (totalling), or balancing accounts. These errors must be located and corrected through proper journal entries, and never by erasing or overwriting the original record.

Golden Rule:

“Errors must be rectified through a rectifying journal entry — not by striking off the wrong entry.”

2. Why Errors Occur in Accounting

Carelessness or lack of attention by the accountant.

Lack of accounting knowledge of the rules of debit and credit.

Heavy workload or fatigue near the end of the accounting year.

Mechanical errors while posting from journal to ledger.

Wrong understanding of the nature of a transaction (capital vs revenue).

Miscommunication between departments providing supporting documents.

3. Types of Errors

Accounting errors are broadly classified into four major categories:

(a) Errors of Omission

When a transaction is completely or partially omitted from the books of accounts.

Complete Omission – the transaction is not recorded at all (does NOT affect Trial Balance).

Partial Omission – only one aspect (debit or credit) is recorded (DOES affect Trial Balance).

Example: Goods sold to Ramesh ₹5,000 not entered in the Sales Book at all → Complete Omission.

(b) Errors of Commission

Errors caused due to wrong posting, wrong casting, wrong balancing, or wrong amounts being recorded.

Wrong amount entered in the Journal or Subsidiary Books.

Wrong totalling (casting) of subsidiary books.

Posting to the wrong side of the correct account.

Posting to a wrong account but on the correct side.

(c) Errors of Principle

When a transaction is recorded in violation of the fundamental principles of accounting — usually by treating capital expenditure as revenue or vice versa.

Example: Purchase of Machinery ₹50,000 wrongly debited to Purchases Account. This violates the principle of capital vs revenue distinction. Such errors do NOT affect the Trial Balance because both sides remain equal.

(d) Compensating Errors

Two or more errors that cancel each other’s effect. The Trial Balance still tallies, hiding the mistakes.

Example: Sales Account is overcast by ₹1,000 and Purchase Account is also overcast by ₹1,000 — both errors compensate each other.

4. Errors Affecting Trial Balance (One-Sided Errors)

These errors affect only one account (one side), so the Trial Balance does NOT tally. They are rectified through the Suspense Account.

Wrong totalling of subsidiary books (Sales Book, Purchase Book, etc.).

Wrong balancing of an account.

Posting of a wrong amount to one account.

Posting to the wrong side of an account.

Omission of posting from journal to ledger.

Posting an amount twice in one account.

5. Errors NOT Affecting Trial Balance (Two-Sided Errors)

These errors involve equal debit and credit aspects, so the Trial Balance still tallies. They are rectified directly without using a Suspense Account.

Errors of complete omission.

Errors of principle.

Compensating errors.

Recording wrong amount in the journal (same amount on both sides).

Posting to a wrong account but on the correct side.

6. Suspense Account

A Suspense Account is a temporary account opened to make the Trial Balance agree when the difference cannot be located immediately. The difference is parked in this account until the errors are discovered and rectified.

Important Rules of Suspense Account:

If the debit side of the Trial Balance is short → Suspense A/c is opened on the debit side.

If the credit side of the Trial Balance is short → Suspense A/c is opened on the credit side.

After all one-sided errors are rectified, the Suspense Account automatically closes.

If a balance still remains in Suspense Account, some errors are yet to be located.

Suspense Account is used only for one-sided errors, NOT for two-sided errors.

7. Solved Problems – Basic Level (No Suspense Account)

In the following problems, the Trial Balance has tallied. Pass rectifying journal entries.

Problem 1 – Error of Complete Omission

Error:

Goods sold to Mohan for ₹4,500 were completely omitted from the books.

Analysis:

No entry was passed at all. Now we simply pass the original entry that should have been recorded.

Rectifying Entry:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Mohan A/c Dr. To Sales A/c(Goods sold to Mohan, omitted earlier, now recorded) | 4,500 | 4,500 |

Problem 2 – Error of Principle

Error:

₹25,000 paid for the purchase of Furniture was wrongly debited to Purchases Account.

Analysis:

Furniture is a capital expenditure (asset) but it was treated as revenue expenditure (Purchases). Furniture A/c should have been debited instead of Purchases A/c.

Rectifying Entry:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Furniture A/c Dr. To Purchases A/c(Furniture purchased wrongly debited to Purchases A/c, now corrected) | 25,000 | 25,000 |

Problem 3 – Posting to Wrong Account (Same Side)

Error:

Cash received from Suresh ₹3,200 was wrongly credited to Naresh’s Account.

Analysis:

Naresh’s A/c was wrongly credited; it should have been Suresh’s A/c. We need to debit Naresh (to cancel) and credit Suresh (to record correctly).

Rectifying Entry:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Naresh A/c Dr. To Suresh A/c(Cash received from Suresh wrongly credited to Naresh, now corrected) | 3,200 | 3,200 |

Problem 4 – Compensating Errors

Error:

Purchases Account was overcast by ₹2,000 and Sales Account was also overcast by ₹2,000.

Analysis:

Both errors cancel each other in the Trial Balance, but the books are still wrong. Reduce both accounts by ₹2,000.

Rectifying Entry:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Sales A/c Dr. To Purchases A/c(Compensating errors in Purchases and Sales A/c rectified) | 2,000 | 2,000 |

Problem 5 – Wrong Amount in Journal

Error:

Goods purchased from Ravi for ₹6,700 were recorded in the Purchases Book as ₹7,600.

Analysis:

Excess of ₹900 (₹7,600 – ₹6,700) was debited to Purchases A/c and credited to Ravi’s A/c. Reverse this excess.

Rectifying Entry:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Ravi A/c Dr. To Purchases A/c(Excess amount of ₹900 wrongly recorded, now reversed) | 900 | 900 |

Page

Rectification of Errors – Class 11 & 12

8. Solved Problems – With Suspense Account

In these problems, the Trial Balance did NOT tally and the difference was placed in a Suspense Account. Pass the rectifying entries and prepare the Suspense Account.

Problem 6 – Single One-Sided Error

Error:

Sales Book was overcast by ₹1,500.

Analysis:

Sales A/c was credited with ₹1,500 extra. Debit Sales A/c to reduce, credit Suspense A/c.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Sales A/c Dr. To Suspense A/c(Sales Book overcast by ₹1,500, now rectified) | 1,500 | 1,500 |

Problem 7 – Wrong Posting (One-Sided)

Error:

Cash paid to Anil ₹2,400 was posted to his account as ₹4,200.

Analysis:

Anil’s A/c was debited with ₹4,200 instead of ₹2,400 — excess debit of ₹1,800. Credit Anil and debit Suspense.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Suspense A/c Dr. To Anil A/c(Excess amount posted to Anil’s A/c now corrected) | 1,800 | 1,800 |

Problem 8 – Omission of Posting

Error:

Discount allowed to Rakesh ₹250 was recorded in the Cash Book but not posted to Rakesh’s Account.

Analysis:

Rakesh’s A/c should have been credited with ₹250. Credit Rakesh and debit Suspense.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Suspense A/c Dr. To Rakesh A/c(Discount allowed not posted to Rakesh’s A/c, now corrected) | 250 | 250 |

Problem 9 – Wrong Side Posting

Error:

₹600 received from Geeta was posted to the debit side of her account instead of the credit side.

Analysis:

Geeta’s A/c was wrongly debited by ₹600. To rectify, we must credit Geeta with ₹1,200 (₹600 to cancel + ₹600 for correct credit), and debit Suspense.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Suspense A/c Dr. To Geeta A/c(Amount received from Geeta wrongly debited, now rectified) | 1,200 | 1,200 |

Problem 10 – Multiple Errors & Suspense Account

Errors Discovered:

Sales Book undercast by ₹800.

Purchases Book overcast by ₹500.

Cash paid to Vimal ₹1,200 not posted to his account.

Discount received ₹150 not posted to Discount Received A/c.

Rectifying Entries:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Suspense A/c Dr. To Sales A/c(Sales Book undercast by ₹800) | 800 | 800 | ||

| Purchases A/c Dr. To Suspense A/c(Purchases Book overcast by ₹500) | 500 | 500 | ||

| Vimal A/c Dr. To Suspense A/c(Cash paid to Vimal not posted) | 1,200 | 1,200 | ||

| Suspense A/c Dr. To Discount Received A/c(Discount received not posted) | 150 | 150 |

Suspense Account:

| Particulars (Dr.) | Amount (₹) | Particulars (Cr.) | Amount (₹) |

| To Sales A/c | 800 | By Purchases A/c | 500 |

| To Discount Received A/c | 150 | By Vimal A/c | 1,200 |

| To Difference (balancing fig.) | 750 | ||

| 1,700 | 1,700 |

The original difference in the Trial Balance was ₹750 (debit short), which has now been fully explained and the Suspense Account closes.

9. Solved Problems – Advanced Level

Problem 11 – Two Errors Combined

Error:

Goods returned by Manoj ₹1,800 were entered in the Returns Outward Book as ₹1,500.

Analysis:

There are TWO mistakes: (1) Goods returned should appear in Returns Inward Book, not Returns Outward Book. (2) Wrong amount ₹1,500 instead of ₹1,800. Both books touch different accounts, so we reverse the wrong entry and pass the correct one.

Rectifying Entry:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Returns Inward A/c Dr.Purchases Returns A/c Dr. To Manoj A/c(Goods returned by Manoj wrongly entered in Returns Outward Book ₹1,500; now corrected to Returns Inward Book ₹1,800) | 1,800 1,500 | 3,300 |

Problem 12 – Capital vs Revenue (Principle)

Error:

₹8,000 spent on the installation of new machinery was debited to the Wages Account.

Analysis:

Installation expenses form part of the cost of the machinery (capital expenditure). Wages A/c was wrongly debited and should be replaced by Machinery A/c.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Machinery A/c Dr. To Wages A/c(Installation cost of machinery wrongly debited to Wages A/c) | 8,000 | 8,000 |

Problem 13 – Multiple Mixed Errors with Suspense

Errors:

Salary paid ₹5,000 was debited to Salary A/c as ₹500.

Goods sold to Pankaj ₹3,400 were recorded in the Sales Book as ₹4,300.

Old furniture sold ₹2,000 was credited to Sales A/c.

Total of Discount Allowed column of Cash Book ₹240 was not posted.

Rectifying Entries:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Salary A/c Dr. To Suspense A/c(Salary ₹5,000 wrongly debited as ₹500; short by ₹4,500) | 4,500 | 4,500 | ||

| Sales A/c Dr. To Pankaj A/c(Goods to Pankaj recorded ₹4,300 instead of ₹3,400; excess ₹900) | 900 | 900 | ||

| Sales A/c Dr. To Furniture A/c(Sale of old furniture wrongly credited to Sales A/c) | 2,000 | 2,000 | ||

| Discount Allowed A/c Dr. To Suspense A/c(Discount Allowed total not posted) | 240 | 240 |

Problem 14 – Effect on Profit

Error:

Repairs to building ₹3,500 were debited to Building Account.

Analysis:

Repairs are a revenue expense. Wrongly capitalising them inflated profit and increased the Building (asset) value. Reverse the asset entry and charge it to Repairs A/c.

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Repairs A/c Dr. To Building A/c(Repairs to building wrongly capitalised, now corrected) | 3,500 | 3,500 |

Effect: Net Profit of the year will decrease by ₹3,500 and Building (asset) will reduce by ₹3,500 in the Balance Sheet.

Problem 15 – Comprehensive Problem

After preparing the Trial Balance, the following errors were detected. Pass rectifying entries and prepare the Suspense Account.

Purchase Book was undercast by ₹600.

Goods worth ₹1,500 distributed as free samples were not recorded.

Cash sales ₹4,200 was recorded in the Sales Book.

Depreciation on machinery ₹1,000 was not posted to the Depreciation A/c.

₹2,500 received from Kavita was credited to Savita’s A/c.

Rectifying Entries:

| Date | Particulars | L.F. | Debit (₹) | Credit (₹) |

| Purchases A/c Dr. To Suspense A/c(Purchase Book undercast by ₹600) | 600 | 600 | ||

| Advertisement (Free Samples) A/c Dr. To Purchases A/c(Goods given as free samples not recorded) | 1,500 | 1,500 | ||

| Cash A/c Dr. To Suspense A/c(Cash sales wrongly recorded in Sales Book, now corrected) | 4,200 | 4,200 | ||

| Depreciation A/c Dr. To Suspense A/c(Depreciation on machinery not posted) | 1,000 | 1,000 | ||

| Savita A/c Dr. To Kavita A/c(Cash received from Kavita wrongly credited to Savita) | 2,500 | 2,500 |

10. Practice Problems

Try solving the following problems on your own. Pass the necessary rectifying journal entries.

Goods sold to Rohit ₹2,800 were not recorded in the books.

Purchase of Computer ₹35,000 was debited to Office Expenses A/c.

Sales Return Book was overcast by ₹450.

A cheque of ₹4,000 received from Deepak was credited to Devesh’s A/c.

Wages paid for installation of plant ₹2,200 were debited to Wages A/c.

Total of Purchase Book ₹15,800 was posted as ₹18,500.

Discount allowed ₹180 was posted to the credit side of Discount Allowed A/c.

Goods withdrawn by the proprietor for personal use ₹1,000 were not recorded.

Bills receivable received from Sandeep ₹6,000 was debited to Bills Payable A/c.

Salary paid in advance ₹2,500 was debited to Salary A/c instead of Prepaid Salary A/c.

11. Exam Tips & Common Mistakes

Always read the question twice — identify whether the Trial Balance has tallied or not. If not, Suspense Account will be involved.

Classify each error first: One-sided (Suspense needed) or Two-sided (no Suspense).

For Errors of Principle, focus on whether the wrong account belongs to Capital or Revenue category.

In wrong-side posting errors, the rectifying amount is DOUBLE the original amount (one to cancel + one to correct).

Always write a clear narration starting with “Being…” or in brackets — examiners deduct marks for missing narration.

After all rectifications, the Suspense Account must close (no balance left). If it doesn’t, recheck the entries.

Effect on Profit: Capital expense wrongly treated as revenue → profit understated. Revenue expense wrongly capitalised → profit overstated.

Use neat, ruled journal format with Date, Particulars, L.F., Debit and Credit columns.

Don’t forget to total both Dr. and Cr. columns of every journal — they must be equal.

Practice atleast 10 mixed problems before the exam to gain speed and accuracy.

12. Quick Summary

| Type of Error | Description | Affects T/B? |

| Complete Omission | Transaction not recorded at all. | No |

| Partial Omission | Only one aspect (Dr or Cr) recorded. | Yes |

| Commission | Wrong amount, wrong account, wrong total. | May or may not |

| Principle | Capital vs revenue treated wrongly. | No |

| Compensating | Two errors cancelling each other. | No |

Remember:

Two-sided errors → rectified by direct journal entry.

One-sided errors → rectified through Suspense Account.

Suspense A/c is temporary — it closes once all errors are located.

Always check the impact on Profit & Loss A/c and Balance Sheet.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.