1. Introduction to Partnership

As a sole proprietor’s business grows, the need for more capital, additional skills, and shared responsibility arises. A single owner often finds it difficult to manage everything alone. To overcome these limitations, two or more persons join hands to run a business together — this form of business organisation is called a Partnership.

Definition (Indian Partnership Act, 1932 – Section 4)

“Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all.”

Features of Partnership

- Two or more persons (Min. 2; Max. 50 as per Companies Act, 2013).

- Agreement (oral or written) between partners.

- Lawful business carried on for profit.

- Sharing of profits and losses in an agreed ratio.

- Mutual agency — every partner is both an agent and a principal.

- Unlimited liability of partners (jointly and severally).

2. Partnership Deed

A Partnership Deed is a written document containing the terms and conditions of partnership, signed by all partners. It helps avoid future disputes.

Contents of a Partnership Deed

- Name and address of the firm and partners

- Nature of business and duration

- Capital contributed by each partner

- Profit/Loss sharing ratio

- Interest on Capital, Drawings, and Loan

- Salary, commission or remuneration to partners

- Rights, duties and powers of partners

- Method of admission, retirement and dissolution

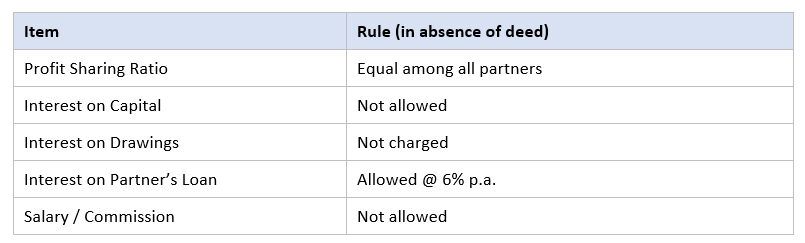

3. Provisions in the Absence of a Partnership Deed

If there is no deed, or the deed is silent on a particular matter, the following rules of the Indian Partnership Act, 1932 apply:

4. Key Terms in Partnership Accounts

Capital Account: The account showing the amount contributed by each partner. It can be maintained under the Fixed Capital Method (Capital A/c + Current A/c) or the Fluctuating Capital Method (only one Capital A/c).

Drawings: Amount or goods withdrawn by a partner from the firm for personal use.

Interest on Capital: Return allowed to a partner on the capital invested. It is an appropriation of profit, not a charge.

Interest on Drawings: Interest charged by the firm from a partner on the amount withdrawn for personal use.

Partner’s Salary / Commission: Remuneration given to active partners as per the deed. Treated as an appropriation of profit.

Profit & Loss Appropriation Account: An extension of the P&L Account showing how net profit is distributed among partners (interest on capital, salary, commission, share of profit, etc.).

Goodwill: The monetary value of a firm’s reputation. It is paid by an incoming partner for the right to share future profits.

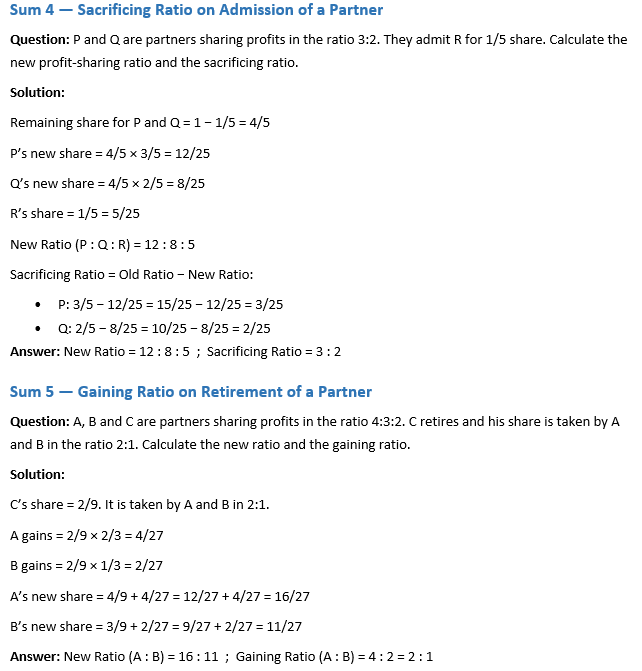

Sacrificing Ratio: The ratio in which old partners surrender their share of profit in favour of a new partner. Sacrificing Ratio = Old Ratio − New Ratio.

Gaining Ratio: The ratio in which the continuing partners gain the share of a retiring/deceased partner. Gaining Ratio = New Ratio − Old Ratio.

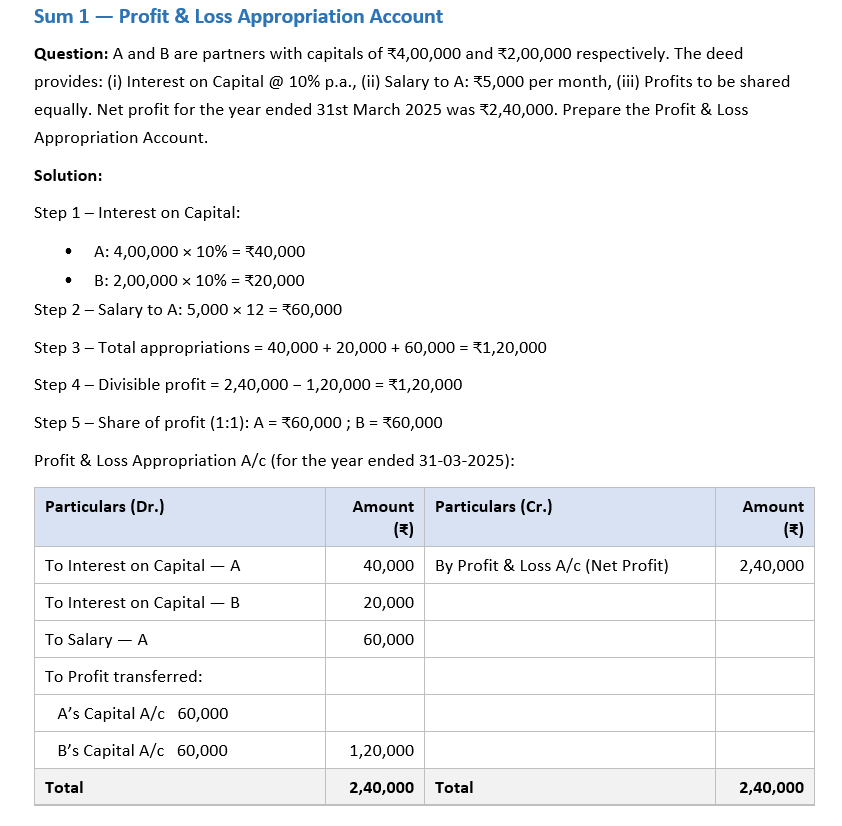

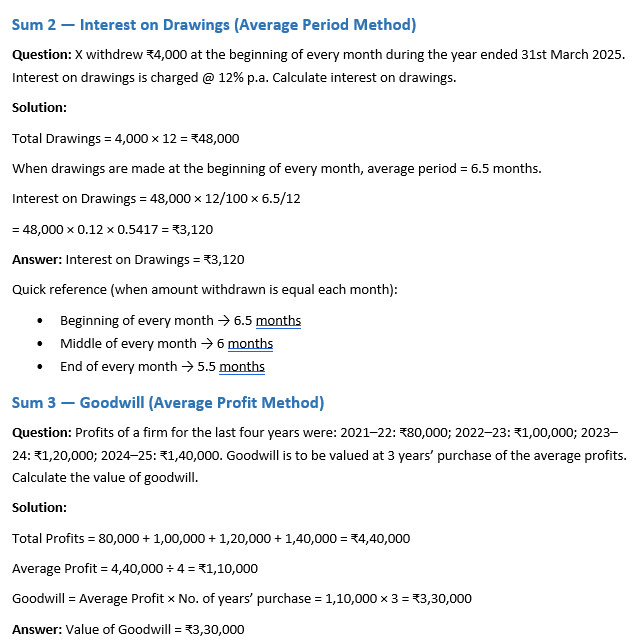

5. Worked Sums

The following solved problems will help you understand how the above concepts are applied in practice.

6. Quick Revision Points

- Partnership = relation between persons sharing profits of a business carried on by all or any of them acting for all.

- Maximum number of partners = 50.

- In absence of deed: equal profits, no IOC, no salary, IOL @ 6% p.a.

- Interest on Capital and Salary are appropriations, not charges.

- Sacrificing Ratio = Old − New; Gaining Ratio = New − Old.

- Goodwill (Average Profit Method) = Average Profit × No. of years purchase.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.