1. What is Admission of a Partner?

When a new partner joins an existing partnership firm to bring in additional capital, skill, or business connections, it is called ‘Admission of a Partner’. As per Section 31 of the Indian Partnership Act, 1932, a new partner cannot be admitted without the consent of all existing partners (unless agreed otherwise).

2. Adjustments Required on Admission

- Calculation of New Profit-Sharing Ratio and Sacrificing Ratio

- Treatment of Goodwill (premium for goodwill)

- Revaluation of Assets and Liabilities

- Distribution of accumulated profits, reserves and losses

- Adjustment of capitals (if required)

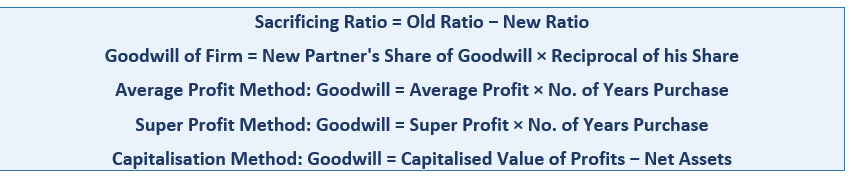

3. Key Formulas — Goodwill

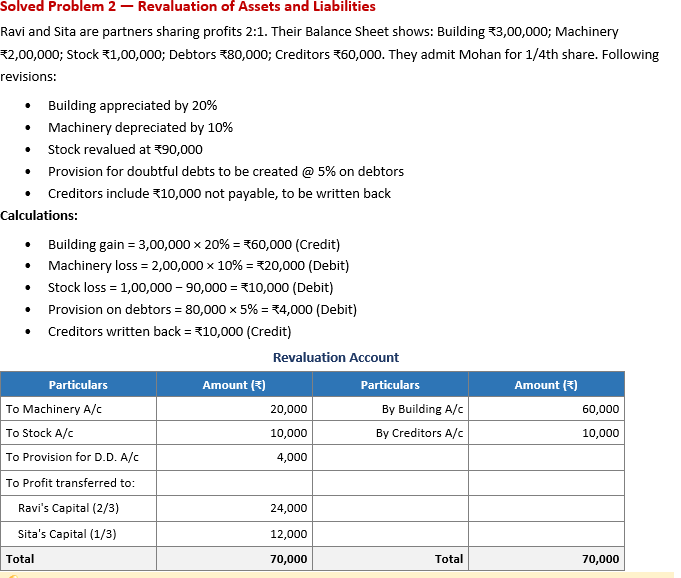

4. Revaluation of Assets and Liabilities

A ‘Revaluation Account’ (also called Profit & Loss Adjustment Account) is prepared. Increase in assets and decrease in liabilities = Credit side (gain). Decrease in assets and increase in liabilities = Debit side (loss). The balancing figure is profit/loss on revaluation, transferred to OLD partners in OLD ratio.

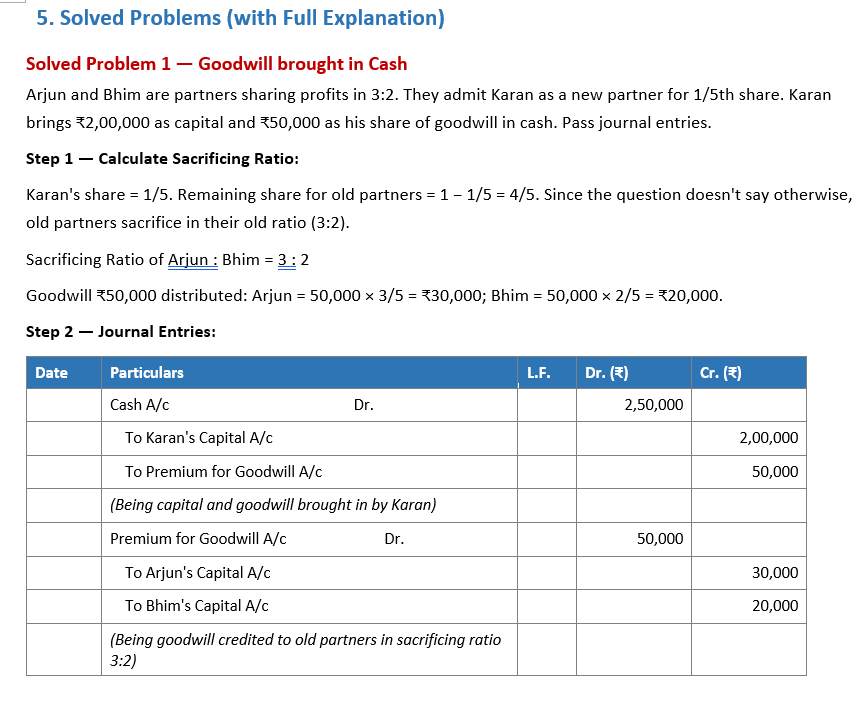

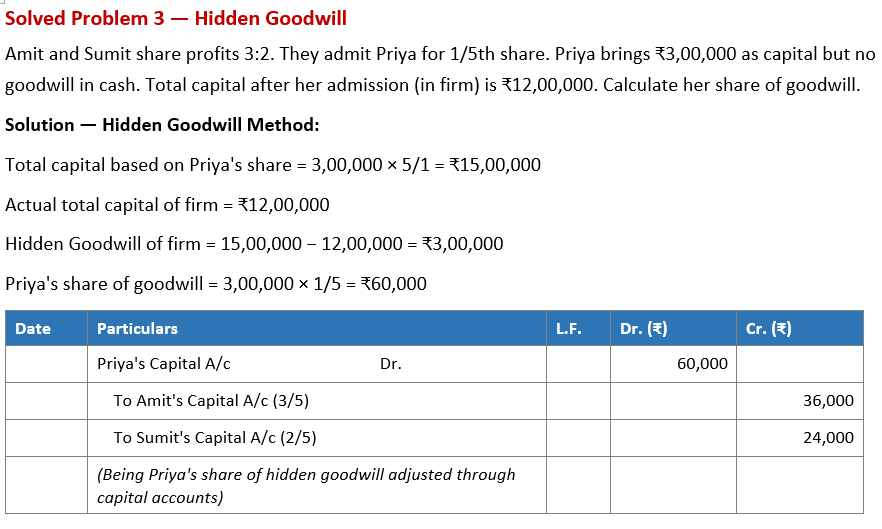

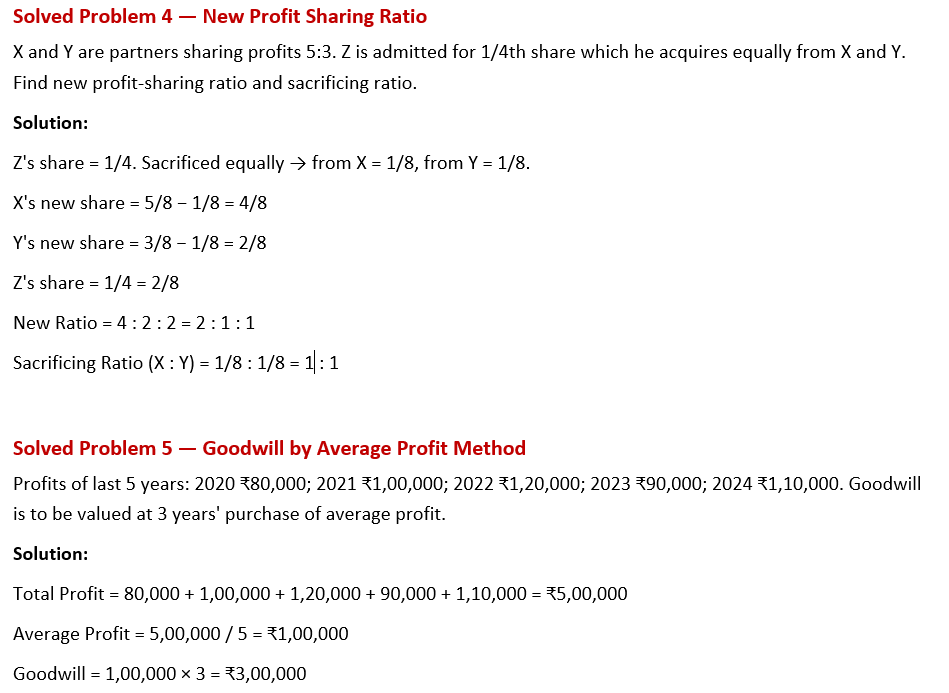

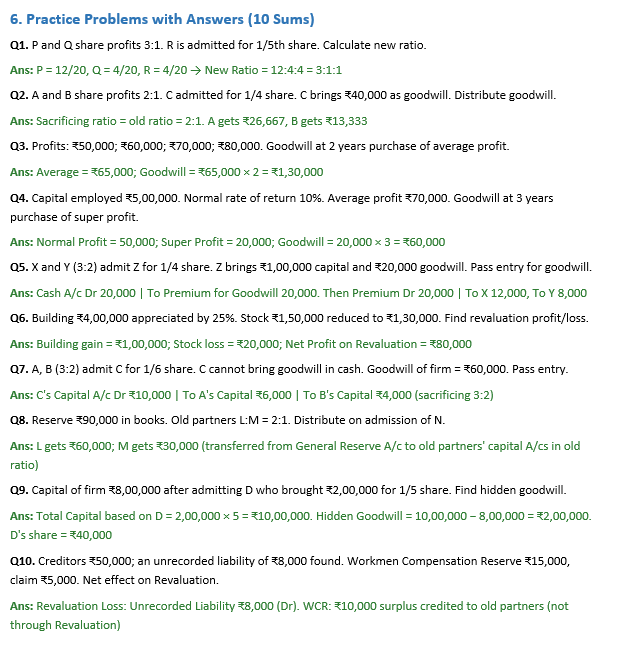

5. Solved Problems (with Full Explanation)

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.