1. Meaning of Retirement

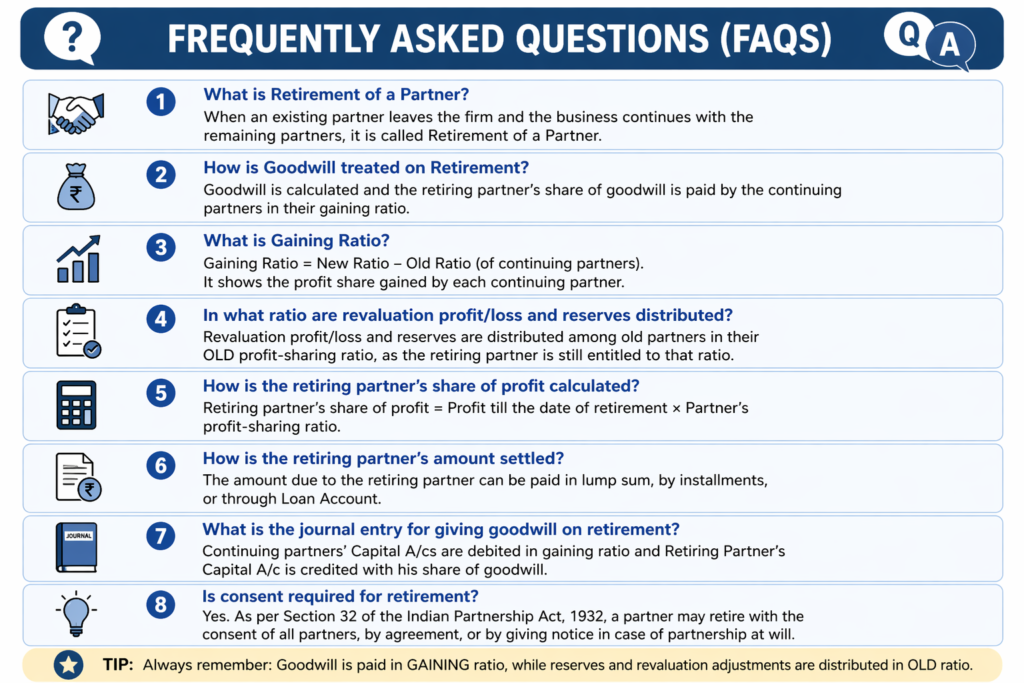

When an existing partner leaves the firm while the business continues with the remaining partners, it is called ‘Retirement of a Partner’. As per Section 32 of the Indian Partnership Act, 1932, a partner may retire (a) with consent of all partners, (b) as per agreement, or (c) by giving notice in case of partnership at will.

2. Adjustments on Retirement

- New profit-sharing ratio and Gaining Ratio of remaining partners

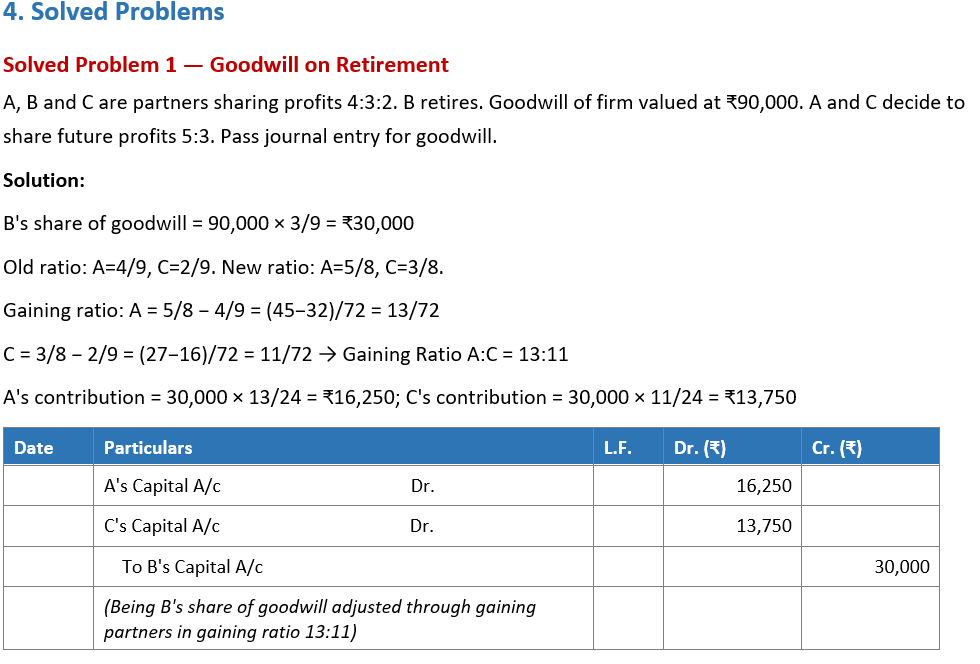

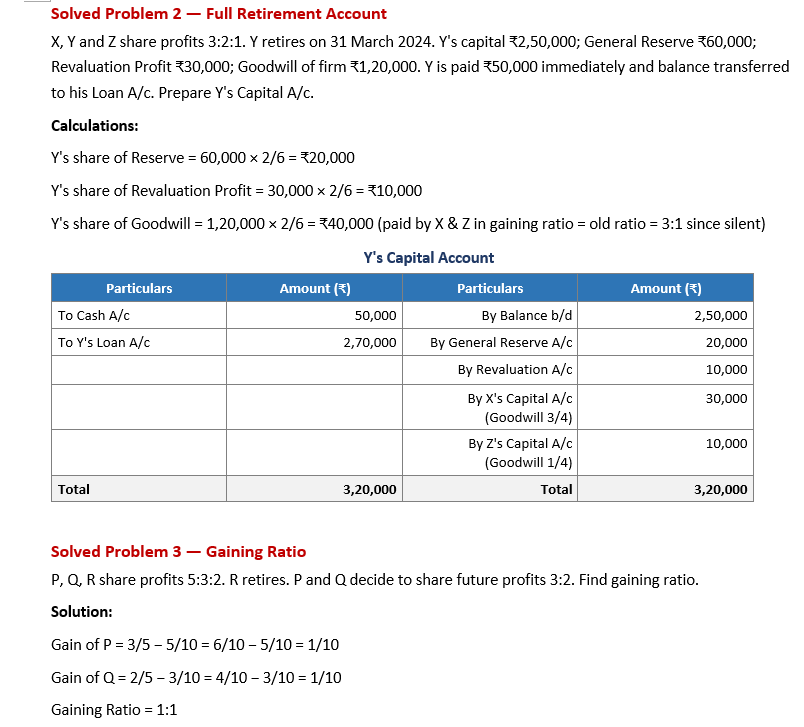

- Treatment of Goodwill (paid by gaining partners to retiring partner)

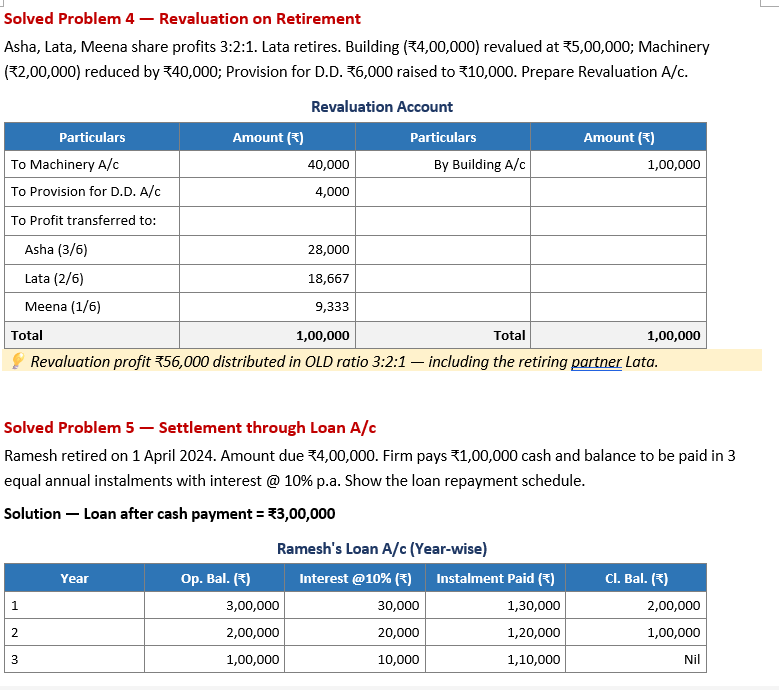

- Revaluation of Assets and Liabilities

- Distribution of Reserves and Accumulated Profits/Losses

- Calculation of share in profit till date of retirement

- Settlement of retiring partner’s account (lump sum / installments / loan)

3. Key Formulas

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.