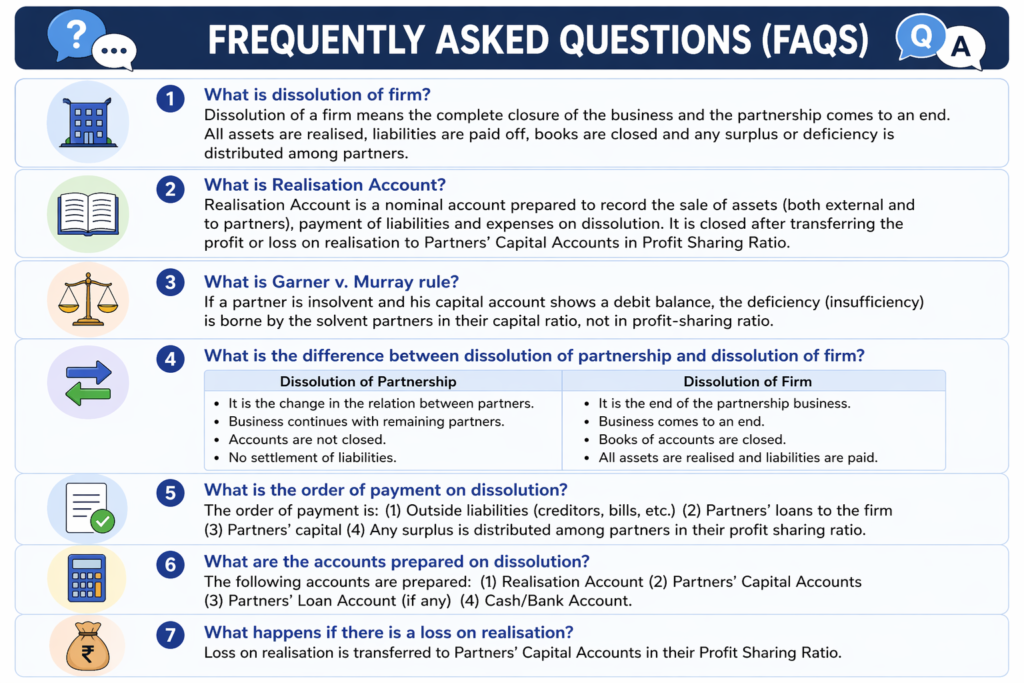

1. Meaning of Dissolution

Dissolution of a Firm means the complete closure of the business. As per Section 39 of the Indian Partnership Act, 1932, dissolution of partnership between all the partners of a firm is called dissolution of the firm. Books are closed, assets are realised (sold), liabilities are paid off, and any surplus/deficiency is distributed among partners.

2. Difference: Dissolution of Partnership vs Dissolution of Firm

| Basis | Dissolution of Partnership | Dissolution of Firm |

| Continuation of business | Business continues | Business ends |

| Books of accounts | Not closed | Closed completely |

| Court intervention | Not required | May be required |

| Settlement of liabilities | Not required | All liabilities settled |

3. Modes of Dissolution

- By Mutual Agreement (Sec. 40)

- Compulsory Dissolution (Sec. 41) — insolvency of all partners or business becoming illegal

- On happening of certain contingencies (Sec. 42) — expiry of term, completion of venture, death, insolvency of partner

- By Notice (Sec. 43) — partnership at will

- By Court Order (Sec. 44) — insanity, misconduct, persistent breach, etc.

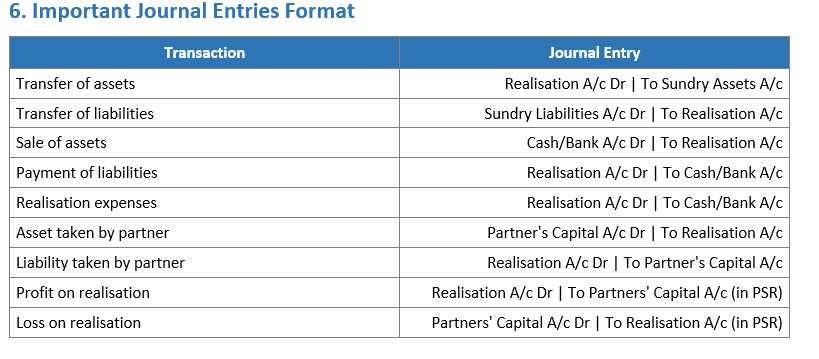

4. Accounts to be Prepared

- Realisation Account — to record sale of assets and payment of liabilities

- Partners’ Capital Accounts

- Partners’ Loan Account (if any)

- Cash / Bank Account

5. Order of Payment (Sec. 48)

- Pay outside debts (creditors, bank loan, etc.)

- Pay partner’s loan to firm

- Pay partner’s capital

- Distribute surplus among partners in profit-sharing ratio

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.