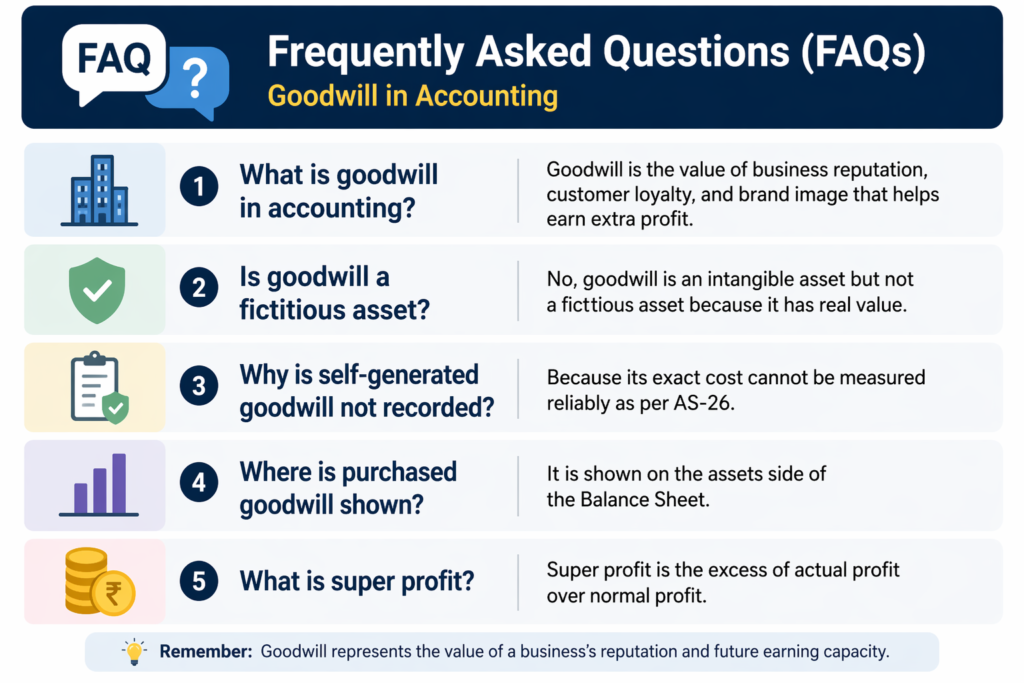

1. Meaning of Goodwill

Goodwill is the monetary value of the reputation, customer loyalty, location advantage, brand image and managerial efficiency that a business builds over time. It is the reason a buyer is willing to pay more than the net asset value of a firm.

In short: Goodwill = the price of a good name. It is what you pay extra because the business is already successful.

2. Definitions by Famous Authors

- Lord Eldon: “Goodwill is the probability that the old customers will resort to the old place.”

- Spicer & Pegler: “Goodwill is the benefit arising from connection and reputation.”

- ICAI (AS-26): Goodwill is an intangible asset which provides future economic benefits.

3. Features (Nature) of Goodwill

- It is an intangible asset — you cannot touch or see it, but it has real value.

- It is not a fictitious asset — unlike preliminary expenses, it has a realisable value.

- Its value is highly subjective — it depends on profits, market conditions and reputation.

- It helps the business earn super profits, i.e., profits more than the normal industry profit.

- It is shown on the assets side of the Balance Sheet only when purchased (AS-26).

4. Why Does Goodwill Exist?

Goodwill exists because some businesses consistently earn more than others operating in the same industry. A few common reasons in the Indian context:

- Brand image — e.g., Tata, Amul, Haldiram’s command extra trust.

- Location — a sweet shop in Chandni Chowk vs an unknown lane.

- Quality of management — TCS and Infosys attract clients due to leadership.

- Long-term customer relationships — your neighbourhood kirana store.

- Patents, licences, exclusive contracts — like a Maruti Suzuki dealership.

5. Types of Goodwill

| Type | Meaning | Recorded in Books? |

| Purchased Goodwill | Paid for at the time of buying a business | Yes |

| Self-Generated Goodwill | Built internally over years of operations | No (per AS-26) |

6. Factors Affecting the Value of Goodwill

- Quality and consistency of profits

- Nature of business — monopoly vs highly competitive

- Location of the business

- Efficiency of management

- Risk involved in the business

- Possession of patents, trademarks, copyrights

- Capital required vs profit earned

7. Need for Valuation of Goodwill

- On admission, retirement or death of a partner

- On change in profit-sharing ratio

- On sale, amalgamation or absorption of business

- On conversion of partnership into a company

- For income tax and wealth tax purposes

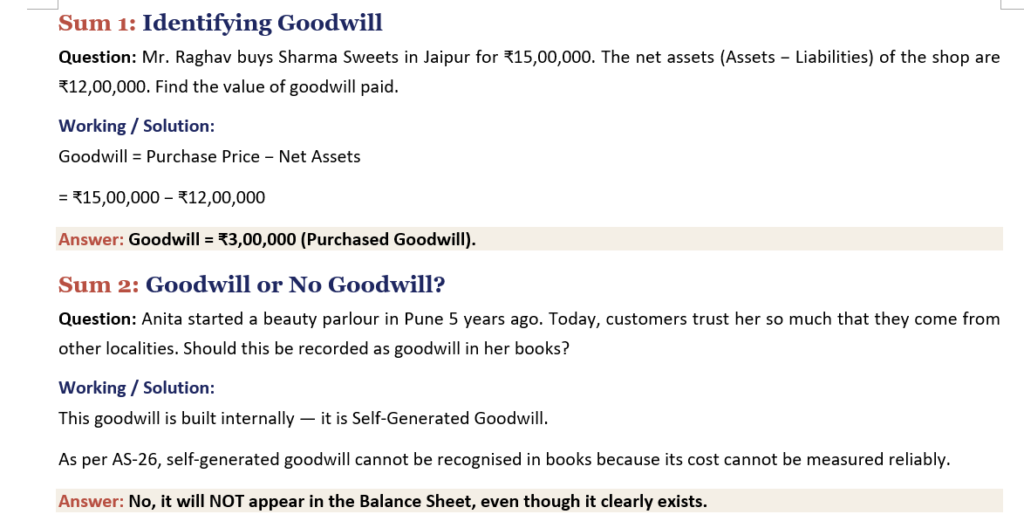

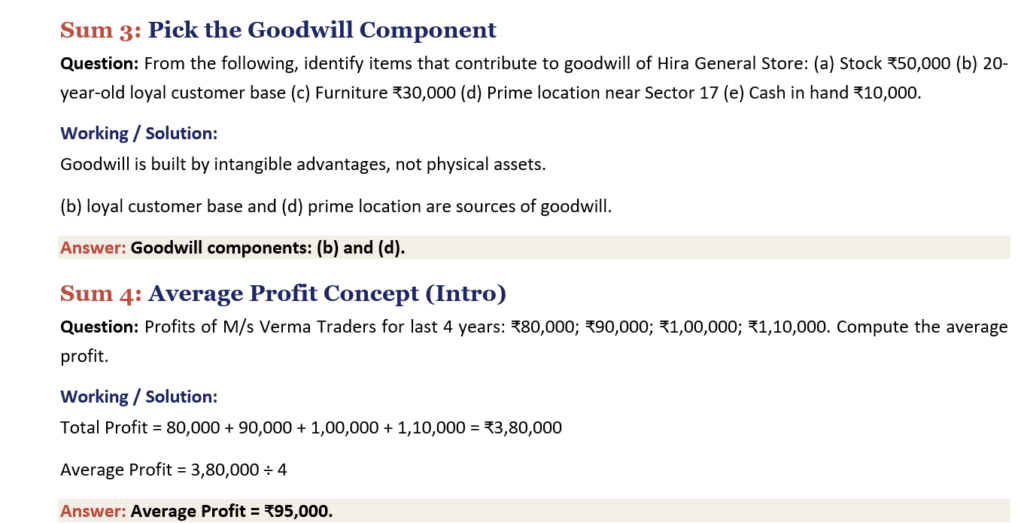

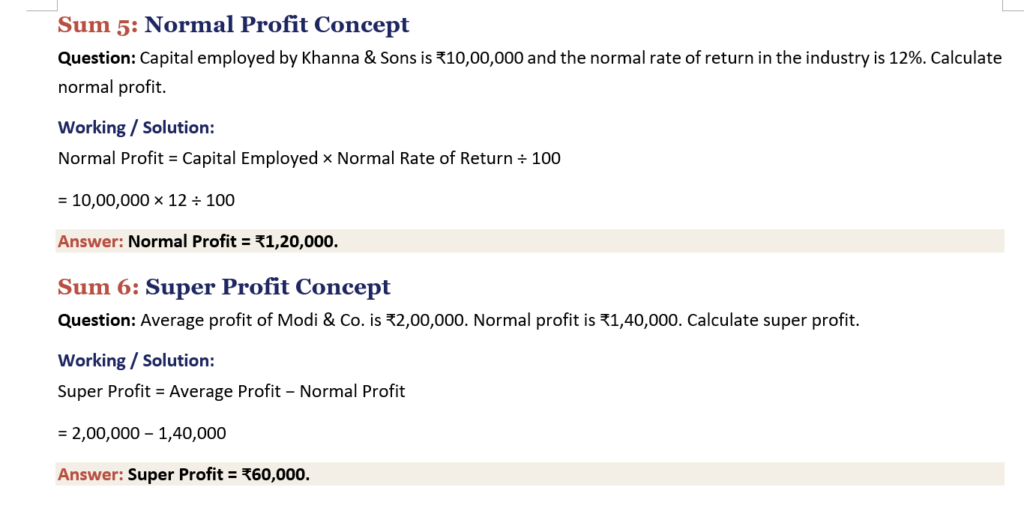

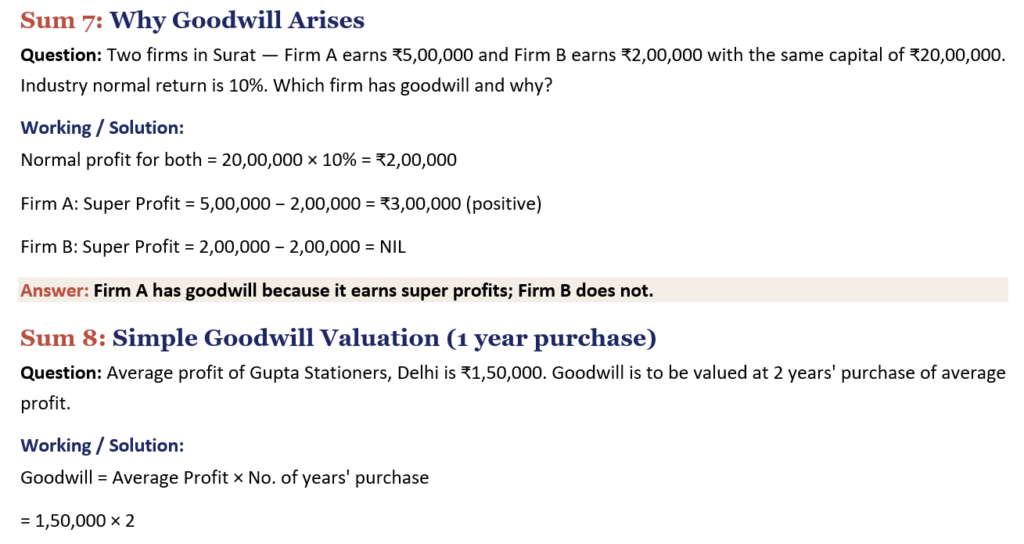

8.Practice Sums (with Solutions)

These sums are framed for Class 11 & 12 students and use small, easy figures so you focus on the concept first.

Key Takeaways

- Goodwill = value of reputation; intangible but real.

- Purchased goodwill is recorded; self-generated is not.

- Super profit is the heart of goodwill — earnings above normal.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.