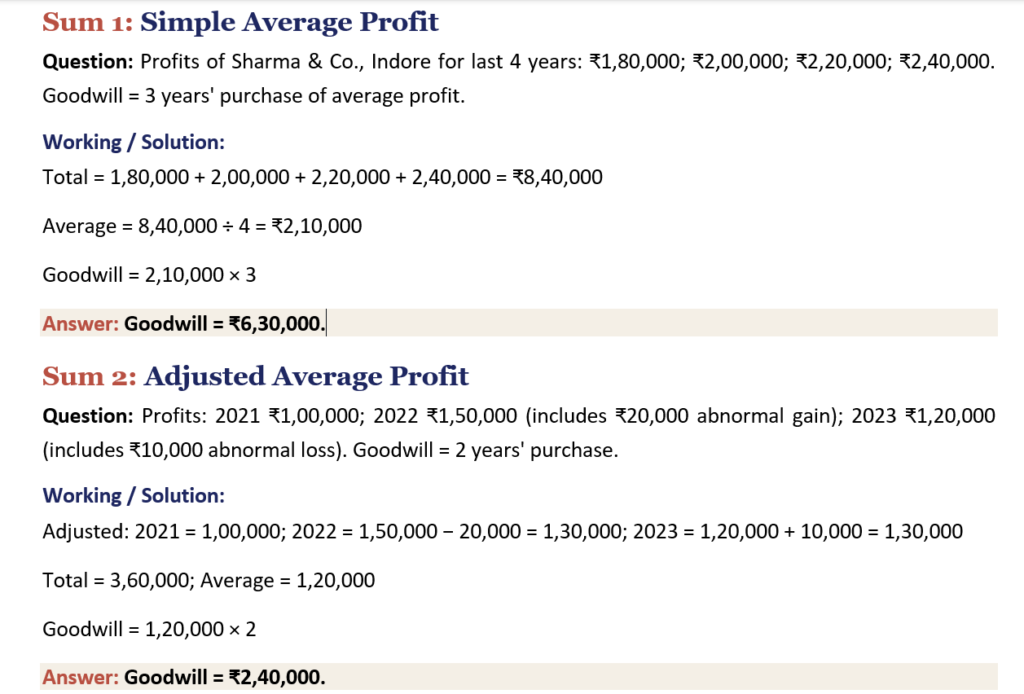

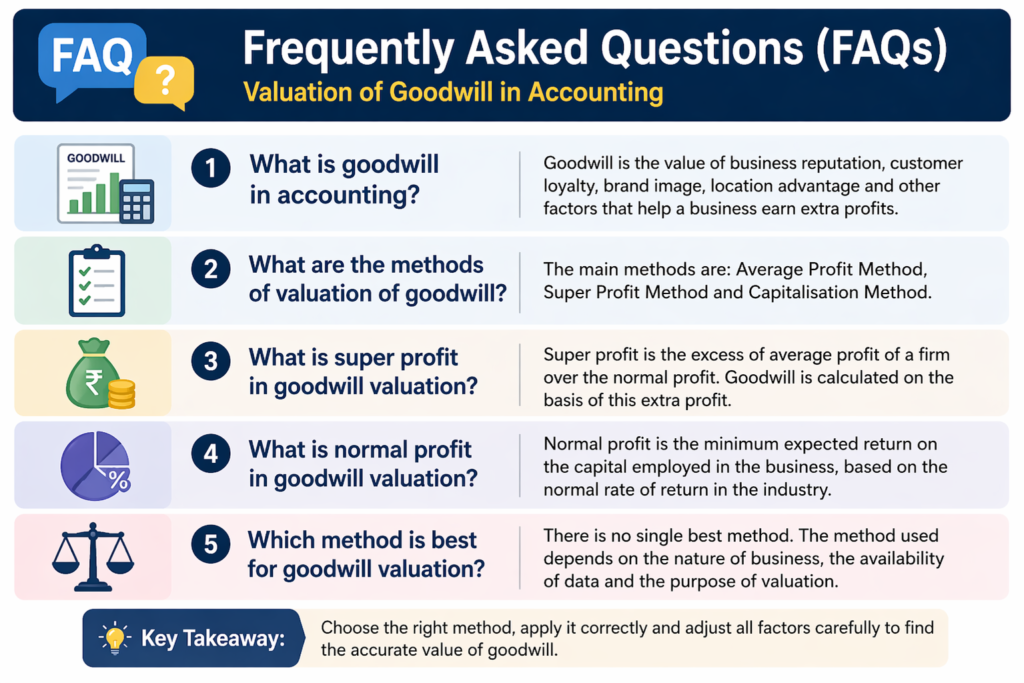

Method 1 : Average Profit Method

Goodwill is calculated as a multiple of the average maintainable profit of past years. Best suited when profits are fairly stable, e.g., a chartered accountant’s firm in Bengaluru.

Goodwill = Average Profit × No. of Years’ Purchase

Steps

- Take last 3–5 years’ profits.

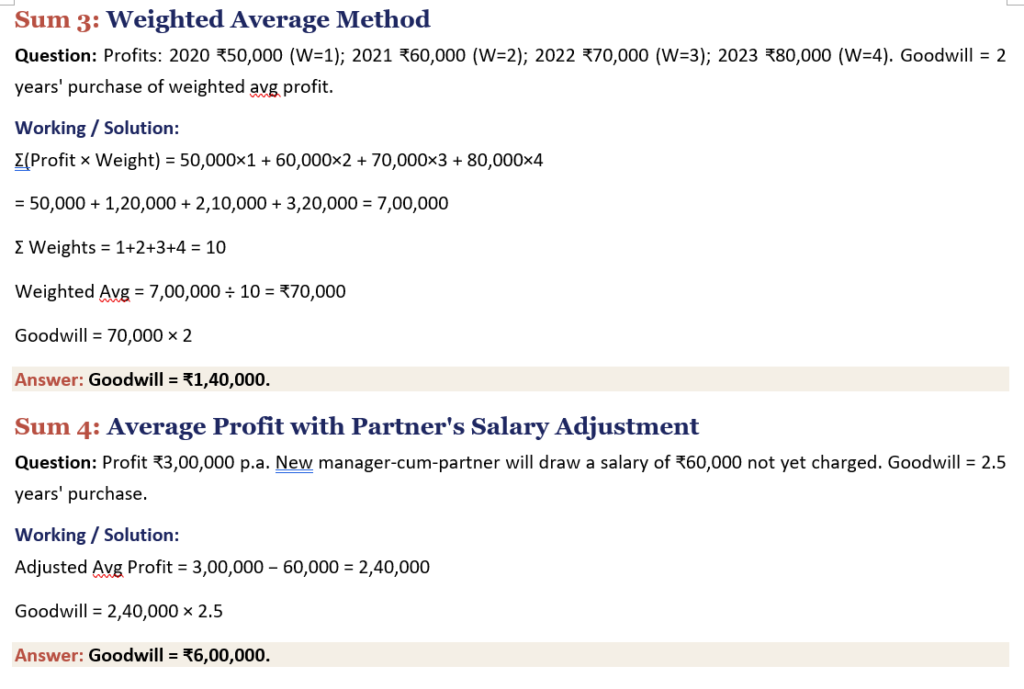

- Adjust for abnormal items (abnormal loss added back; abnormal gains deducted; partner’s salary deducted, etc.).

- Find the simple or weighted average.

- Multiply by the agreed number of years’ purchase.

Weighted Average Method

When recent profits are more important (e.g., growing IT firm), assign higher weights to recent years.

Weighted Avg Profit = Σ(Profit × Weight) ÷ Σ(Weights)

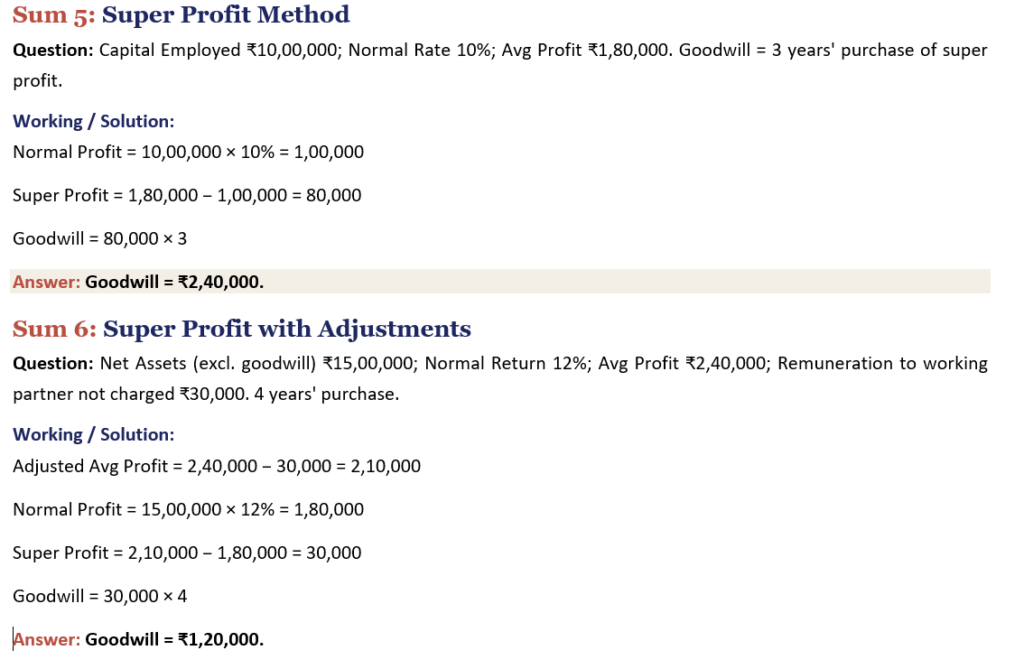

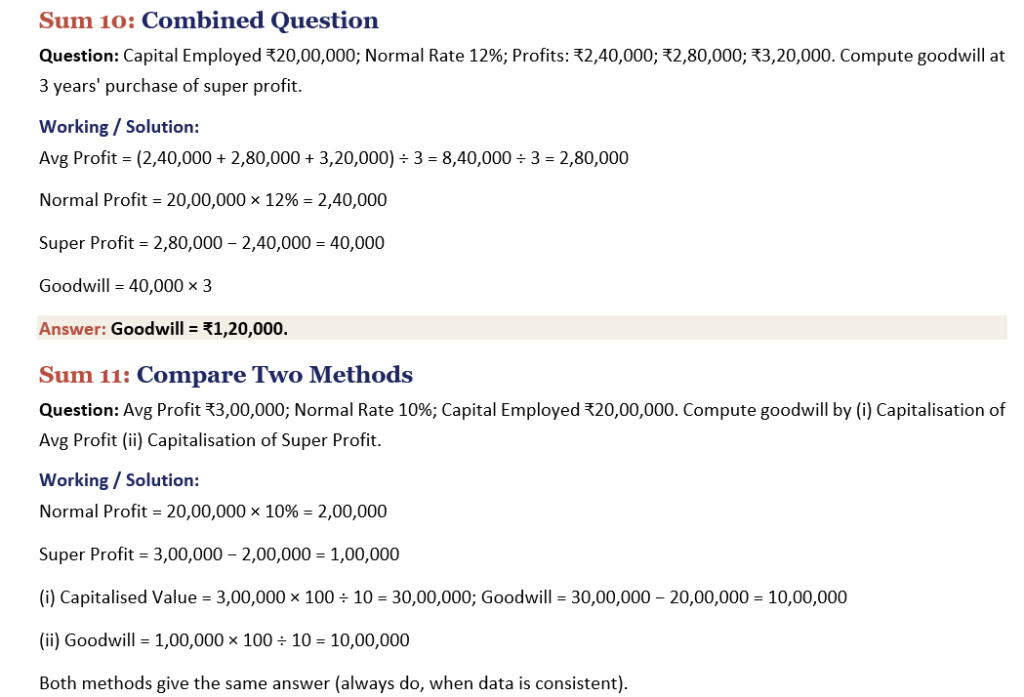

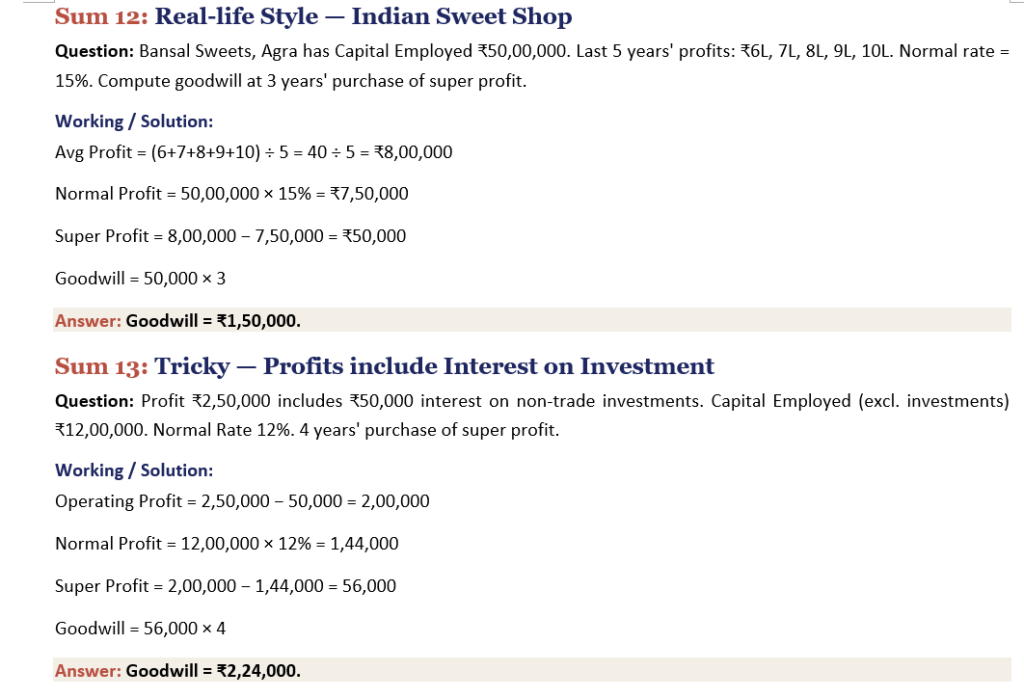

Method 2 : Super Profit Method

Goodwill is paid for the extra-ordinary earning capacity. If a firm only earns the normal industry profit, no buyer will pay anything beyond net assets. Hence we focus on Super Profit.

Super Profit = Avg Profit − Normal Profit

Goodwill = Super Profit × No. of Years’ Purchase

Where: Normal Profit = Capital Employed × Normal Rate of Return ÷ 100

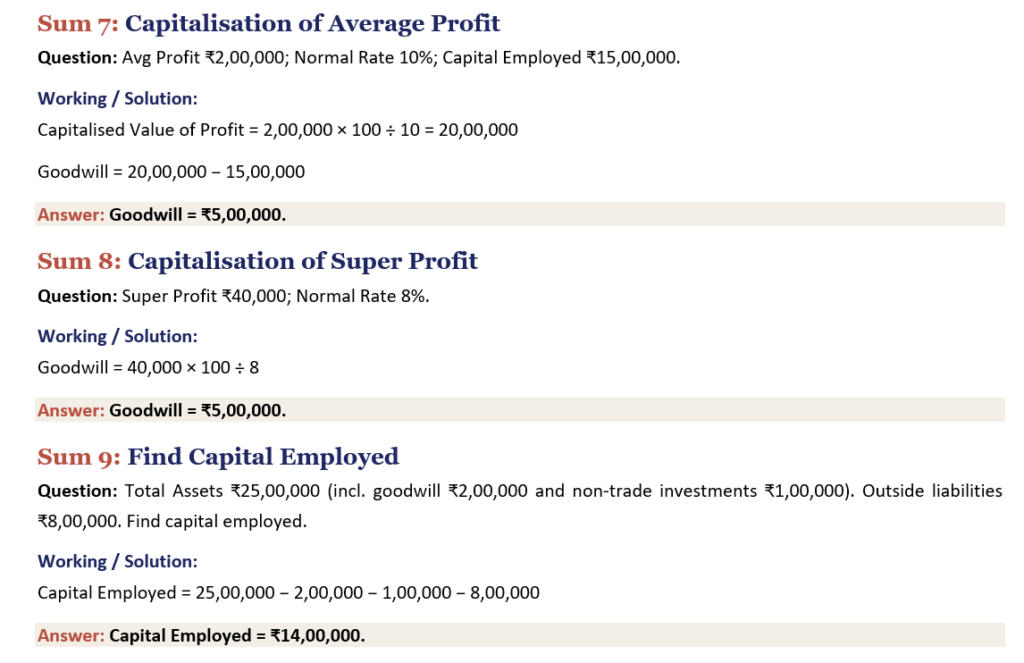

Method 3 : Capitalisation Methods

(a) Capitalisation of Average Profit

Capitalised Value = Avg Profit × 100 ÷ Normal Rate

Goodwill = Capitalised Value − Net Assets (Capital Employed)

(b) Capitalisation of Super Profit

Goodwill = Super Profit × 100 ÷ Normal Rate

Capital Employed — How to Compute

- Capital Employed = All Assets (excluding goodwill, fictitious assets, non-trade investments) − Outside Liabilities.

- Or: Capital Employed = Capital + Reserves + P&L (Cr.) − Fictitious Assets.

Quick Comparison

| Basis | Average Profit | Super Profit | Capitalisation |

| Focus | Whole profit | Excess profit | Total earning capacity |

| Easy? | Easiest | Moderate | Toughest |

| Use | Stable firms | Growing firms | Negotiation / sale |

Practice Sums (with Full Solutions)

Examiner’s Tips

- Always adjust profits BEFORE averaging.

- Exclude goodwill, fictitious assets and non-trade investments from capital employed.

- Read carefully: “years’ purchase” means multiplication, not interest.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.