AS-26 Rule You Must Remember

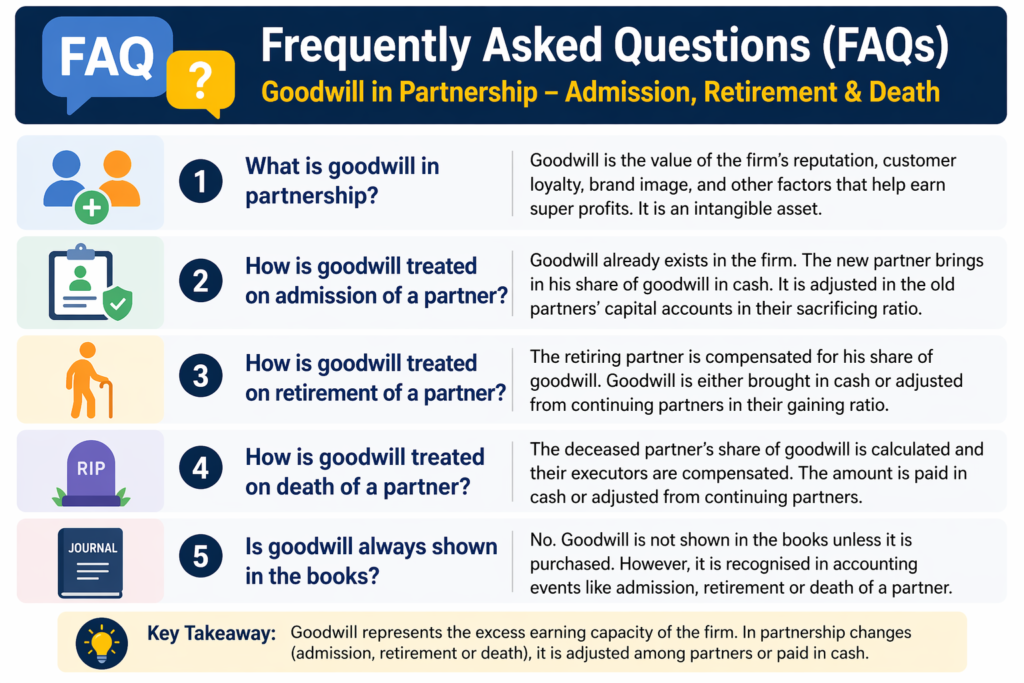

Golden rule: Goodwill is never raised and kept in the books. It is adjusted only through Partners’ Capital Accounts in the gaining/sacrificing ratio.

1. Treatment on Admission of a Partner

When a new partner joins, old partners sacrifice a part of their share. The new partner brings goodwill (premium) to compensate them.

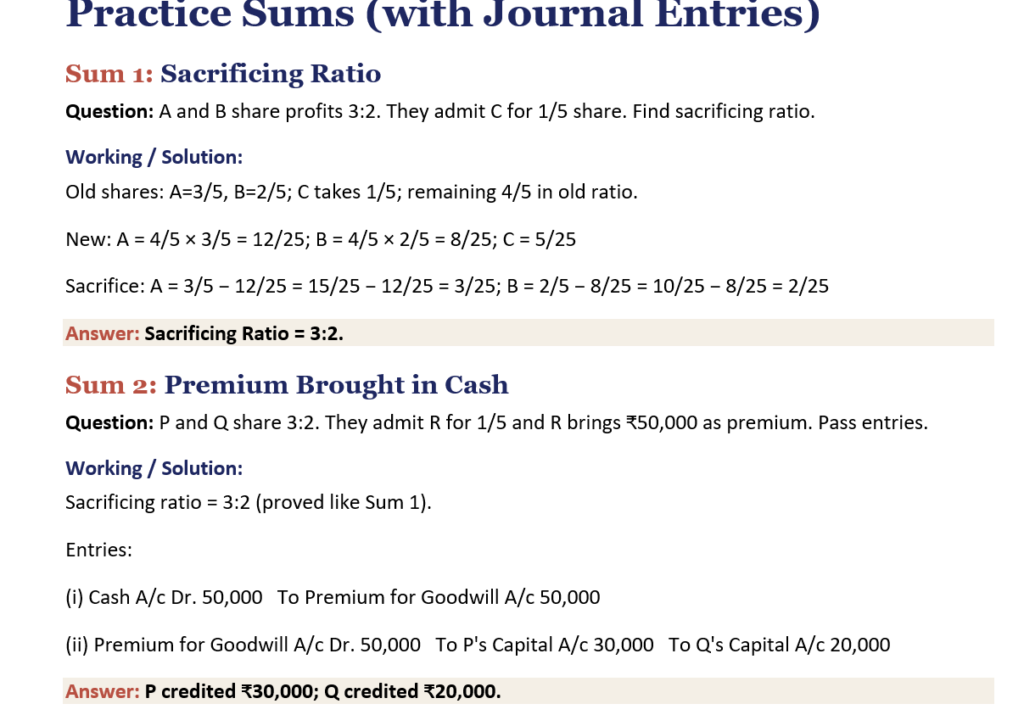

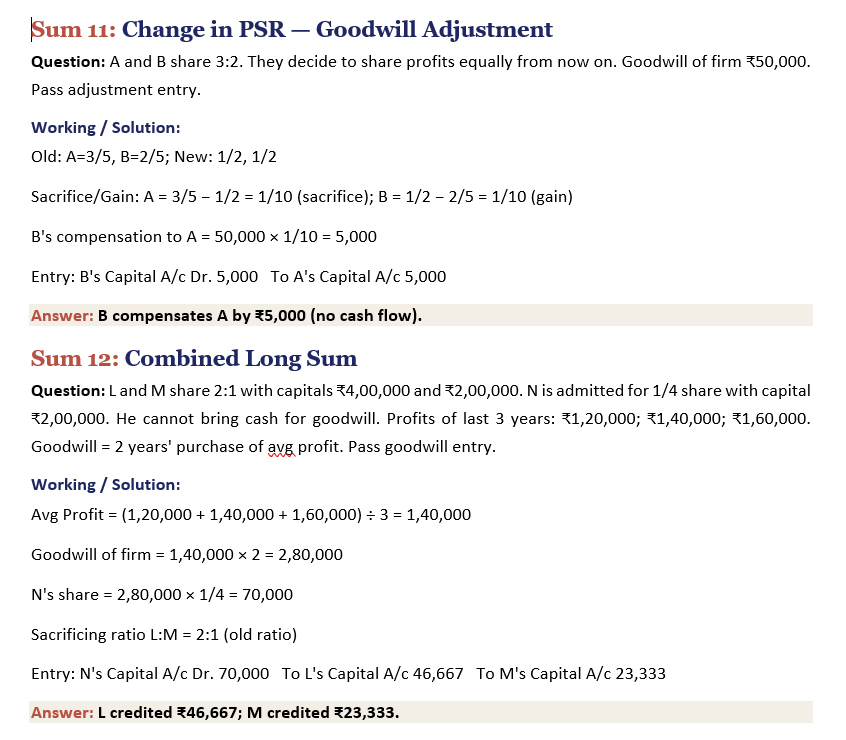

Sacrificing Ratio

Sacrificing Ratio = Old Share − New Share

Case A — New Partner Brings Goodwill in Cash

Journal Entries:

- Cash A/c Dr. To Premium for Goodwill A/c — (premium received)

- Premium for Goodwill A/c Dr. To Old Partners’ Capital A/cs (in sacrificing ratio)

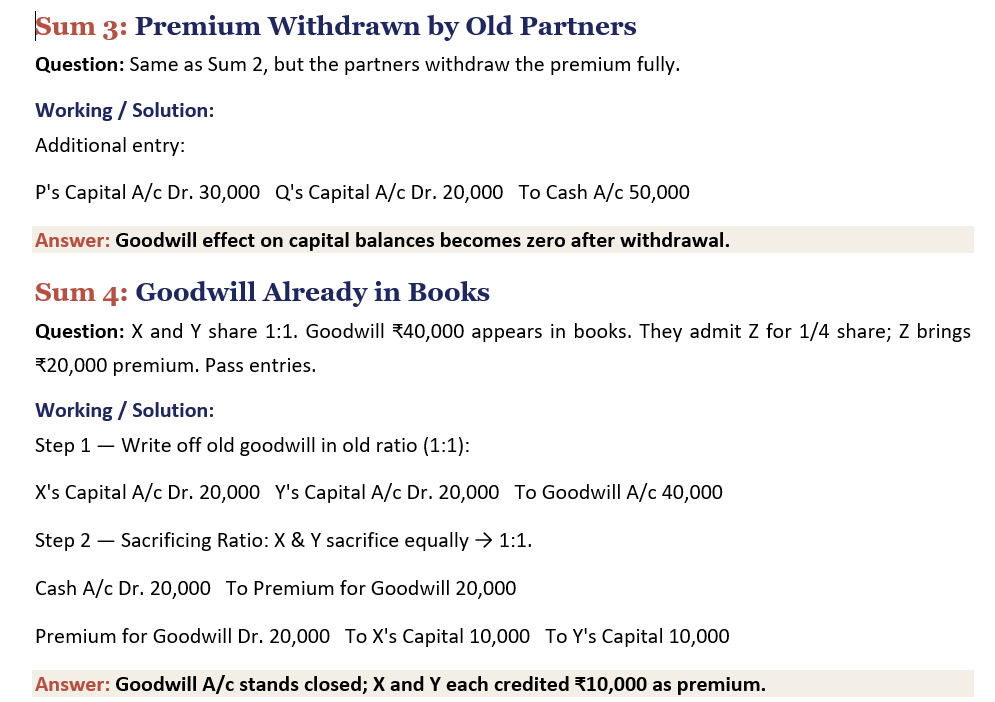

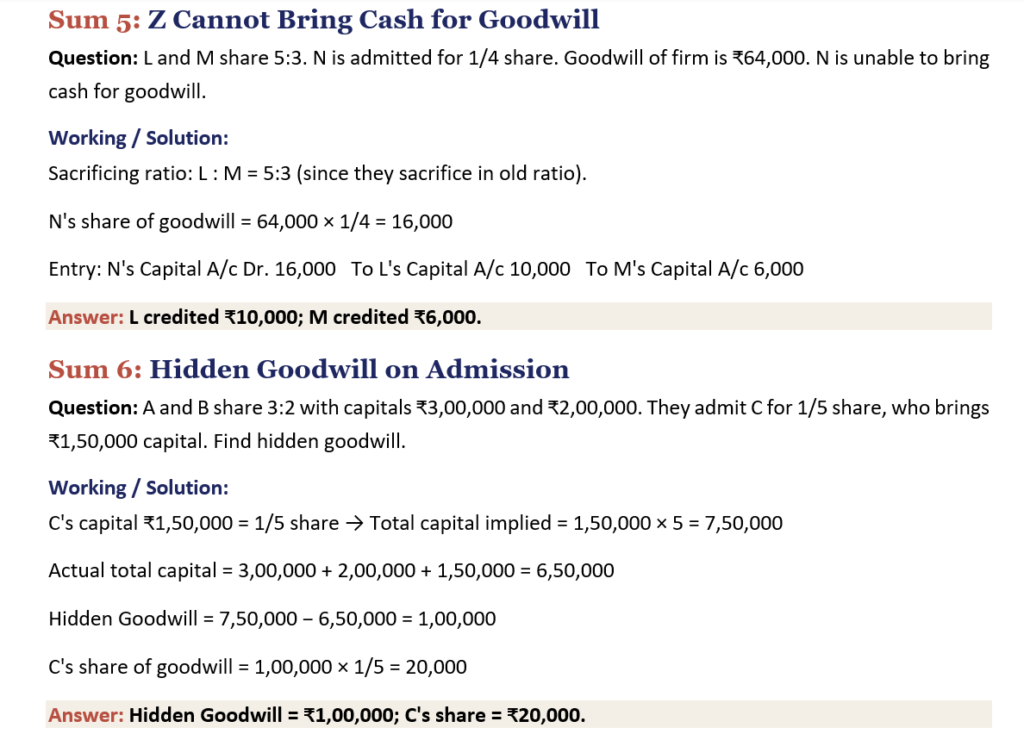

Case B — New Partner Cannot Bring Goodwill

- New Partner’s Capital A/c Dr. To Old Partners’ Capital A/cs (in sacrificing ratio)

Case C — Goodwill Already Appears in Books

- First write off existing goodwill: Old Partners’ Capital A/cs Dr. (old ratio) To Goodwill A/c

- Then make the normal premium entry.

2. Treatment on Retirement / Death of a Partner

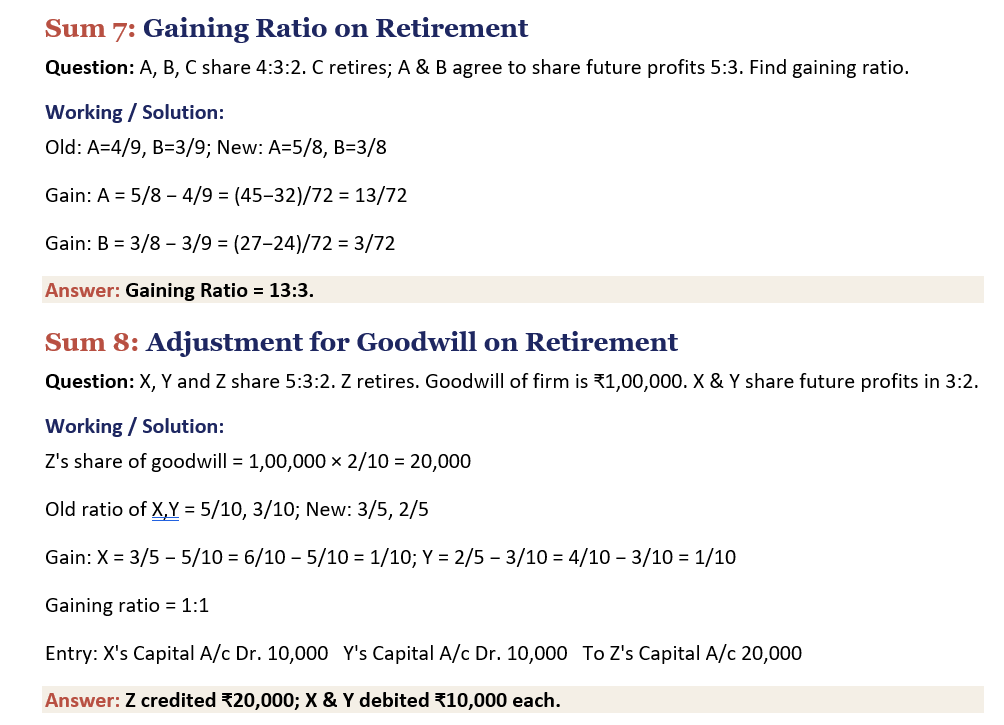

Gaining Ratio

Gaining Ratio = New Share − Old Share

Adjustment Entry (no cash):

- Remaining Partners’ Capital A/cs Dr. (in gaining ratio) To Retiring/Deceased Partner’s Capital A/c (his share of goodwill)

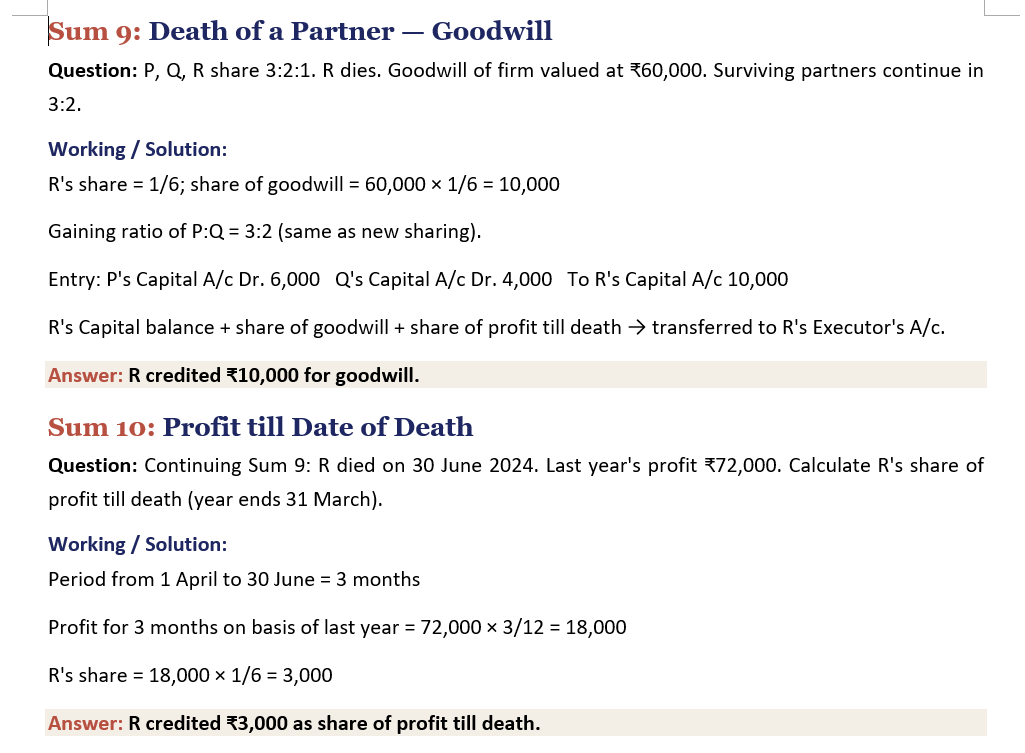

In Case of Death

- Profit till date of death is calculated and credited to deceased partner’s capital account.

- The amount payable is transferred to his Executor’s A/c.

Hidden Goodwill

If the question gives you the amount of capital brought by the new partner and the new profit-sharing ratio, but does not mention goodwill, calculate hidden goodwill:

Hidden Goodwill = (New Partner’s Capital × Reciprocal of his share) − Total Capital of new firm

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.