Introduction

In financial accounting and financial management, both the Cash Flow Statement and Fund Flow Statement are important tools used to analyze the financial position of a business. Although both statements deal with the movement of funds, they differ in purpose, concept, and analysis. Understanding these differences helps students, managers, investors, and businesses make better financial decisions.

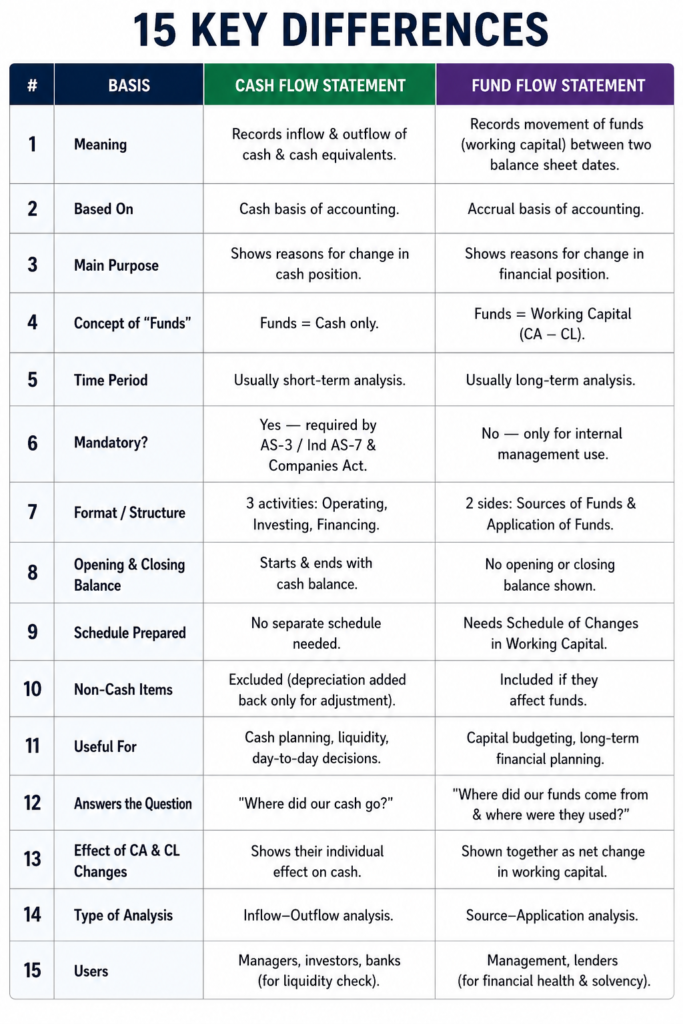

Meaning of Cash Flow Statement

A Cash Flow Statement is a financial statement that records the inflow and outflow of cash and cash equivalents during a particular accounting period. It shows how cash is generated and utilized through operating, investing, and financing activities.

The main purpose of the cash flow statement is to analyze the liquidity and cash position of a business and determine whether the company has enough cash to meet its short-term obligations.

Meaning of Fund Flow Statement

A Fund Flow Statement is a financial statement that shows the movement of funds (working capital) between two balance sheet dates. It explains the sources from which funds are obtained and the areas where those funds are utilized.

The main purpose of the fund flow statement is to analyze changes in the financial position and working capital of a business over a period of time.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.