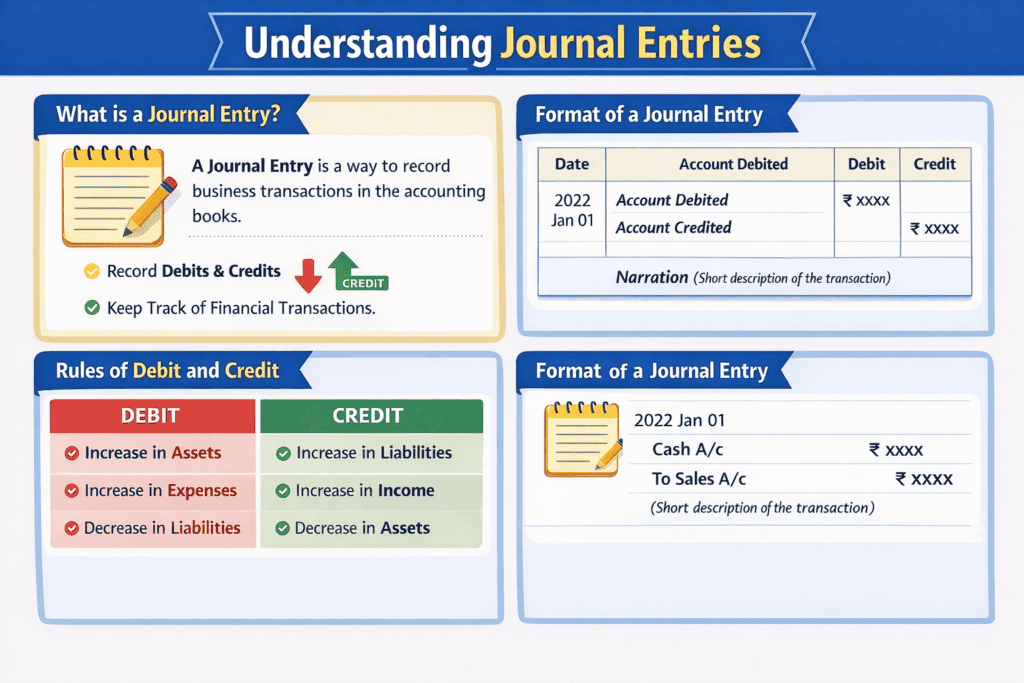

What is Journal Entry

Every time a business spends or earns money, someone has to write it down precisely, consistently, and correctly. That’s exactly what a journal entry does. In simple term, Journal entry is a formal note that records who gave what, who received what, and why.

Definition

“A journal is a book of original entry in which business transactions are recorded in chronological order, showing the accounts to be debited and credited.”

– L.C. Cropper

Example: Journal Entry in Accounting

Imagine you buy a laptop for your business for ₹50,000 cash.

In your personal life, you just think, “I spent 50k.” In accounting, you have to show the give and take:

- The Take: You gained an Asset (the Laptop).

- The Give: You lost an Asset (the Cash).

The Journal Entry would look like this:

| Date | Account Name | Debit (In) | Credit (Out) |

|---|---|---|---|

| April 7 | Laptop (Asset) | ₹50,000 | |

| Cash (Asset) | ₹50,000 |

It follows one golden rule: every transaction has two sides – one Debit, one Credit. They must always be equal!

Steps to understanding journal Entries

Step 1: Identify the Three Types of Accounts

To make a journal entry, you first look at a transaction and ask: “Which of these three is involved?”

- Real Accounts (Assets/Things): These are things you can touch or own (Cash, Furniture, Buildings, Stock).

- Personal Accounts (People/Firms): These are names of people or companies (Rahul, HDFC Bank, Suppliers, Customers).

- Nominal Accounts (Expenses & Income): These are things you can’t touch only experiences (Rent, Salary, Interest, Sales, Purchases).

Step 2: Apply the “Golden Rules”

Once you identify the account type, apply the specific rule for that bucket:

| Account Type | Rule for Debit (Dr.) | Rule for Credit (Cr.) |

|---|---|---|

| Real | What Comes In | What Goes Out |

| Personal | The Receiver | The Giver |

| Nominal | All Expenses & Losses | All Incomes & Gains |

Practice with a “Service” Example

1. Business Started with Cash ₹5,00,000

- Accounts: Cash (Real) and Capital (Personal – represents the Owner).

- Rules: Cash is coming in (Debit); the Owner is the giver (Credit).

- Entry:

Cash A/c …. Dr. ₹5,00,000

To Capital A/c …. ₹5,00,000

2. Purchased Furniture for Cash ₹20,000

- Accounts: Furniture (Real) and Cash (Real).

- Rules: Furniture comes in (Debit); Cash goes out (Credit).

- Entry:

Furniture A/c …. Dr. ₹20,000

To Cash A/c …. ₹20,000

3. Purchased Goods for Cash ₹50,000

- Accounts: Purchases (Nominal/Expense) and Cash (Real).

- Rules: Purchases is an expense (Debit); Cash goes out (Credit).

- Entry:

Purchases A/c …. Dr. ₹50,000

To Cash A/c …. ₹50,000

4. Purchased Goods from M/s Gupta & Co. on Credit ₹30,000

- Accounts: Purchases (Nominal) and M/s Gupta & Co. (Personal).

- Rules: Purchases is an expense (Debit); Gupta & Co. is the giver (Credit).

- Entry:

Purchases A/c …. Dr. ₹30,000

To M/s Gupta & Co. A/c …. ₹30,000

5. Sold Goods for Cash ₹40,000

- Accounts: Cash (Real) and Sales (Nominal/Income).

- Rules: Cash comes in (Debit); Sales is an income (Credit).

- Entry:

Cash A/c …. Dr. ₹40,000

To Sales A/c …. ₹40,000

6. Sold Goods to Amit on Credit ₹15,000

- Accounts: Amit (Personal) and Sales (Nominal).

- Rules: Amit is the receiver (Debit); Sales is an income (Credit).

- Entry:

Amit’s A/c …. Dr. ₹15,000

To Sales A/c …. ₹15,000

7. Paid Office Rent ₹5,000 by Cash

- Accounts: Rent (Nominal) and Cash (Real).

- Rules: Rent is an expense (Debit); Cash goes out (Credit).

- Entry:

Rent A/c …. Dr. ₹5,000

To Cash A/c …. ₹5,000

8. Deposited Cash into HDFC Bank ₹1,00,000

- Accounts: Bank (Personal) and Cash (Real).

- Rules: Bank is the receiver (Debit); Cash goes out (Credit).

- Entry:

Bank A/c …. Dr. ₹1,00,000

To Cash A/c …. ₹1,00,000

9. Withdrew Cash for Personal Use ₹2,000

- Accounts: Drawings (Personal – Owner) and Cash (Real).

- Rules: Owner is the receiver of benefit (Debit); Cash goes out (Credit).

- Entry:

Drawings A/c …. Dr. ₹2,000

To Cash A/c …. ₹2,000

10. Paid Cash to M/s Gupta & Co. ₹30,000

- Accounts: M/s Gupta & Co. (Personal) and Cash (Real).

- Rules: Gupta & Co. is the receiver (Debit); Cash goes out (Credit).

- Entry:

M/s Gupta & Co. A/c …. Dr. ₹30,000

To Cash A/c …. ₹30,000

Try these 5 problems yourself:

- Bought furniture for office ₹20,000 cash

- Received rent from tenant ₹5,000

- Paid electricity bill ₹2,000

- Sold goods to Mahesh on credit ₹40,000

- Withdrawn cash from bank ₹15,000

Answers to Practice Problems

- Furniture A/c Dr / To Cash A/c

- Cash A/c Dr / To Rent Received A/c

- Electricity A/c Dr / To Cash A/c

- Mahesh A/c Dr / To Sales A/c

- Cash A/c Dr / To Bank A/c

Identify the Account Type → Apply the Golden Rule → Pass the Journal Entry

Remember this simple formula:

Mastering journal entries is the first step towards learning accounting, ledger posting, trial balance, and final accounts.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.