If the Journal is a diary where you write everything as it happens, the Ledger is a set of folders. Each folder (Account) contains only transactions related to one specific person, asset, or expense.

Definition:

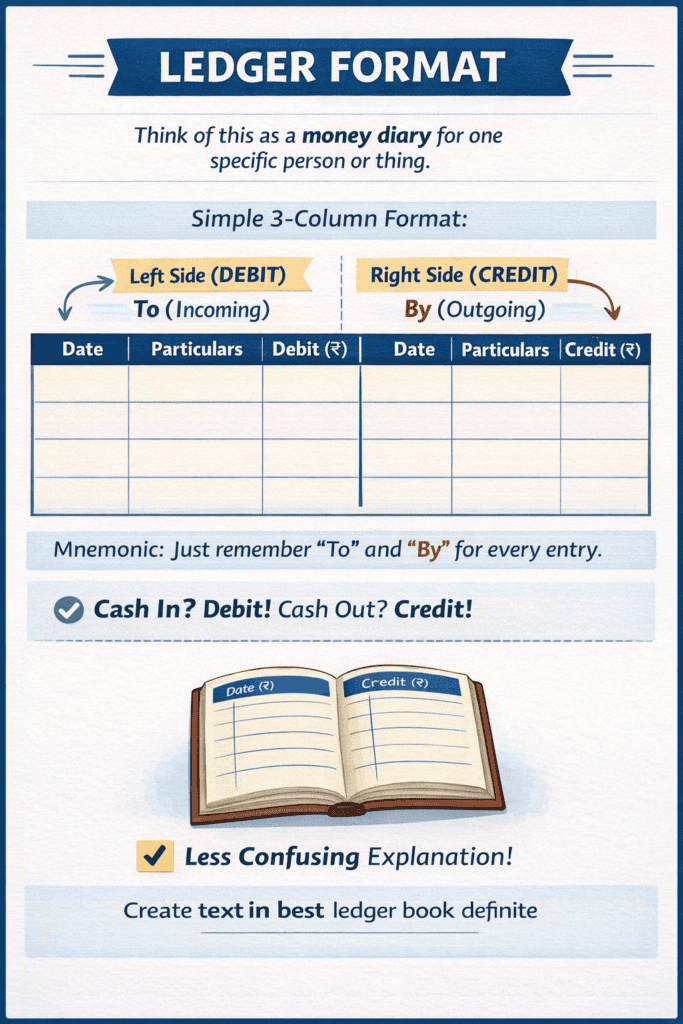

A Ledger is the “Principal Book of Accounts” where transactions are classified and summarized into individual accounts.

Format of ledger

Think of a Ledger as a “Money Diary” for one specific person or thing.

- Left Side (Debit – Dr): Think of this as the “Incoming” or “Receiver” side.

- Right Side (Credit – Cr): Think of this as the “Outgoing” or “Giver” side.

The Visual Template (Use this for every account)

| Date | Who/Why (Particulars) | Ref (JF) | Amount (₹) | Date | Who/Why (Particulars) | Ref (JF) | Amount (₹) |

|---|---|---|---|---|---|---|---|

| LEFT SIDE (DEBIT) | Start with “To“ | RIGHT SIDE (CREDIT) | Start with “By“ |

15 Practice Sums (Step-by-Step Solutions)

To make this “Pro” level, I will show you the Journal Entry first (The logic), then the Ledger (The recording).

Sum 1: Starting Business

Transaction: Started business with Cash ₹5,00,000.

- Logic: Cash is coming in (Debit), Capital is the source (Credit).

- Journal: Cash A/c (Dr) to Capital A/c (Cr).

Cash Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 1 | To Capital A/c | 1 | 5,00,000 |

Capital Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 1 | By Cash A/c | 1 | 5,00,000 |

Sum 2: Bank Deposit

Transaction: Deposited ₹2,00,000 into Bank.

- Logic: Bank receives (Debit), Cash goes out (Credit).

Bank Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 2 | To Cash A/c | 1 | 2,00,000 |

Cash Account (Continued)

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 1 | To Capital A/c | 1 | 5,00,000 | April 2 | By Bank A/c | 1 | 2,00,000 |

Sum 3: Cash Purchase

Transaction: Bought goods for Cash ₹50,000.

- Logic: Purchases (Expense) is Debit, Cash (Going out) is Credit.

Purchases Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 3 | To Cash A/c | 1 | 50,000 |

Sum 4: Cash Sale

Transaction: Sold goods for Cash ₹80,000.

- Logic: Cash (Coming in) is Debit, Sales (Income) is Credit.

Sales Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 4 | By Cash A/c | 1 | 80,000 |

Sum 5: Paying Rent (Expense)

Transaction: Paid Rent ₹10,000 by Cash.

Rent Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 5 | To Cash A/c | 1 | 10,000 |

Sum 6: Credit Purchase (Buying on “Udhaar”)

Transaction: Bought goods from Anita on credit ₹40,000.

- Logic: Purchases (Debit), Anita is the Giver (Credit).

Anita’s Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 6 | By Purchases A/c | 1 | 40,000 |

Sum 7: Credit Sale

Transaction: Sold goods to Rahul on credit ₹60,000.

Rahul’s Account

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 7 | To Sales A/c | 1 | 60,000 |

Sum 8 & 9: Returns (The Reverse Logic)

Transaction 8: Returned goods to Anita worth ₹2,000.

Transaction 9: Rahul returned goods to us worth ₹3,000.

Purchase Returns A/c (Sum 8)

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 8 | By Anita’s A/c | 1 | 2,000 |

Sales Returns A/c (Sum 9)

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 9 | To Rahul’s A/c | 1 | 3,000 |

Sum 10 & 12: Settlements & Discounts (The “MBA” Level)

Sum 12 Transaction: Rahul owed us ₹57,000. He paid ₹55,000 and we gave him a ₹2,000 discount.

Rahul’s Account (Settlement)

| Date | Particulars | JF | Amount (₹) | Date | Particulars | JF | Amount (₹) |

|---|---|---|---|---|---|---|---|

| April 7 | To Sales | 60,000 | April 9 | By Sales Return | 3,000 | ||

| April 12 | By Cash A/c | 55,000 | |||||

| April 12 | By Discount A/c | 2,000 | |||||

| Total | 60,000 | Total | 60,000 | ||||

| (Look! The total matches, so Rahul’s account is now closed). |

Sum 11, 13, 14, 15: Special Adjustments

- Sum 11 (Compound): Started business with Cash and Furniture. You open two ledger accounts and post “To Capital” in both.

- Sum 13 (Drawings): Owner took money for personal use. Drawings A/c (Dr) To Bank (Cr).

- Sum 14 (Depreciation): Value of Furniture went down. Depreciation A/c (Dr) To Furniture A/c (Cr).

- Sum 15 (Outstanding): Salary is due but not paid. Salary A/c (Dr) To Outstanding Salary A/c (Cr).

Practice Section: 5 Sums for You

| Sum No. | Date | Transaction Description | Difficulty |

|---|---|---|---|

| 1 | April 1 | Started business with Cash ₹2,00,000. | Basic |

| 2 | April 5 | Purchased Furniture for Cash ₹20,000. | Basic |

| 3 | April 10 | Bought Goods from “Modern Traders” on Credit ₹15,000. | Intermediate |

| 4 | April 15 | Sold Goods to “Kiran” on Credit ₹25,000. | Intermediate |

| 5 | April 20 | Paid Cash to “Modern Traders” ₹10,000. | Intermediate |

Answer Key (The Step-by-Step Solution)

For each sum, I will show you which two accounts are affected and where the money goes.

Sum 1: Capital Entry

- Accounts affected: Cash A/c and Capital A/c.

- The Logic: Cash comes in (Debit), Capital is the source (Credit).

Cash Account

| Date | Particulars | Amount (₹) | Date | Particulars | Amount (₹) |

|---|---|---|---|---|---|

| April 1 | To Capital A/c | 2,00,000 |

Sum 2: Asset Purchase

- Accounts affected: Furniture A/c and Cash A/c.

- The Logic: Furniture comes in (Debit), Cash goes out (Credit).

Furniture Account

| Date | Particulars | Amount (₹) | Date | Particulars | Amount (₹) |

|---|---|---|---|---|---|

| April 5 | To Cash A/c | 20,000 |

Sum 3: Credit Purchase (The “Liability”)

- Accounts affected: Purchases A/c and Modern Traders A/c.

- The Logic: Goods come in (Debit), Modern Traders is the Giver/Creditor (Credit).

Modern Traders Account

| Date | Particulars | Amount (₹) | Date | Particulars | Amount (₹) |

|---|---|---|---|---|---|

| April 10 | By Purchases A/c | 15,000 |

Sum 4: Credit Sale (The “Asset/Debtor”)

- Accounts affected: Kiran’s A/c and Sales A/c.

- The Logic: Kiran is the Receiver (Debit), Sales is the Income (Credit).

Kiran’s Account

| Date | Particulars | Amount (₹) | Date | Particulars | Amount (₹) |

|---|---|---|---|---|---|

| April 15 | To Sales A/c | 25,000 |

Sum 5: Paying a Creditor

- Accounts affected: Modern Traders A/c and Cash A/c.

- The Logic: Modern Traders receives money (Debit), Cash goes out (Credit).

Modern Traders Account (Updated)

| Date | Particulars | Amount (₹) | Date | Particulars | Amount (₹) |

|---|---|---|---|---|---|

| April 20 | To Cash A/c | 10,000 | April 10 | By Purchases A/c | 15,000 |

| Balance c/d | 5,000 | ||||

| Total | 15,000 | Total | 15,000 |

(Note: The “Balance c/d” shows we still owe them ₹5,000).

Tips and tricks

5 simple “Golden Tricks” to master ledger posting without any confusion:

- The “Opposite Name” Trick

Inside any account, never write its own name. If you are in the Cash Account, look at the journal and grab the other name (like Sales or Rent) and write that instead. It’s like a “No Selfies” rule! - The “To” & “By” Shortcut

Remember: “To” is Left, “By” is Right.

If the journal entry has a “To” (the credit part), it ironically moves to the Left side of the other account. If it’s the top name (the debit part), it moves to the Right side of the other account using “By.” - The Cash “Plus/Minus” Hack

For Cash or Bank accounts:- Left side is your (+) Plus side (Money coming in).

- Right side is your (-) Minus side (Money going out).

If you paid someone, it’s always on the Right. If you received money, it’s always on the Left.

- The “Best Friends” Rule (Discounts)

Cash and Discount are best friends; they always stay on the same side. If you post Cash on the Left side, the Discount Allowed goes on the Left side too. They never leave each other. - The “Slide” Balancing Trick

When finishing an account, the “Balance c/d” is just a gap-filler on the smaller side. To start the next month, just “Slide” that amount to the opposite side below the total line and call it “Balance b/d.” That is your real final answer.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.