When you maintain a Cash Book in your accounts, your bank also maintains a Pass Book (Bank Statement) for you. Both books record the same transactions — but sometimes their balances do not match.

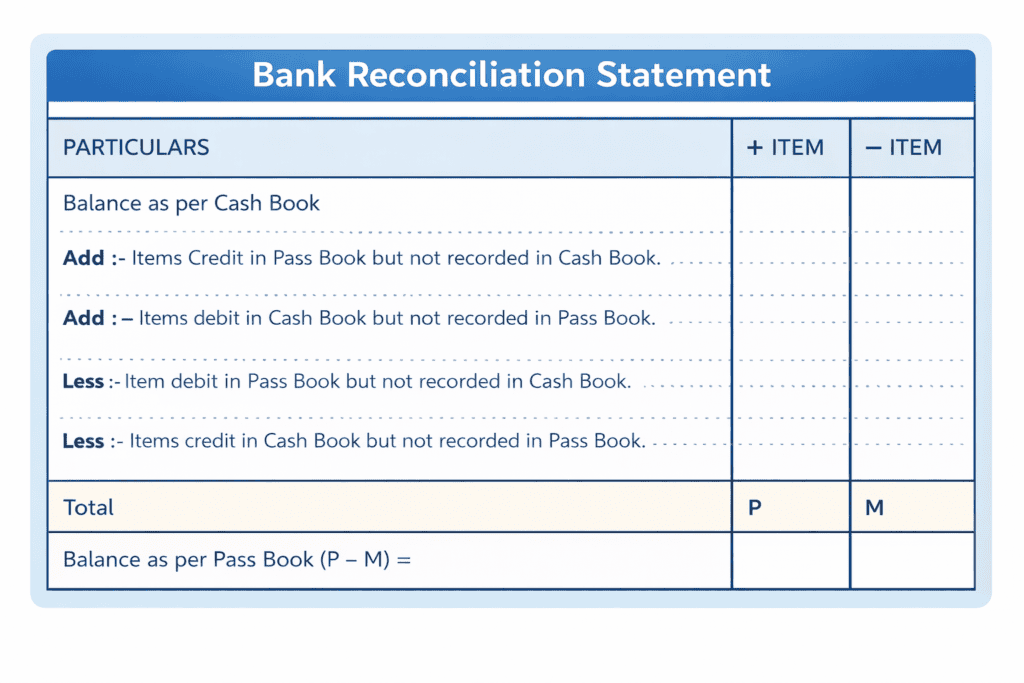

The statement prepared to explain the difference between Cash Book balance and Pass Book balance is called the Bank Reconciliation Statement (BRS).

Simple Definition: BRS = A statement that bridges the gap between Cash Book balance and Pass Book balance.

Why Do the Two Balances Differ?

There are 3 main categories of reasons:

Category 1 — Time Gap Reasons (Most Common)

Situation

Who Records First?

Why Difference?

Cheque issued but recipient has not gone to bank yet

Only Cash Book (Cr.)

Bank does not know yet

Cheque deposited but bank has not cleared it yet

Only Cash Book (Dr.)

Bank processing pending

Category 2 — Bank Acts Without Telling You

Situation

Who Records First?

Bank deducts charges

Only Pass Book

Bank credits interest

Only Pass Book

Bank collects cheque/bill on your behalf

Only Pass Book

Bank pays insurance/loan EMI directly

Only Pass Book

Customer deposits directly into your account

Only Pass Book

Cheque deposited dishonoured (bounced)

Only Pass Book

Category 3 — Errors (Tricky — Exam Favourite!)

Type of Error

Where it Happens

Wrong amount recorded

Cash Book or Pass Book

Entry recorded twice

Cash Book or Pass Book

Entry completely missed

Cash Book or Pass Book

Casting mistake (addition error)

Cash Book

Cheque recorded in CB but never sent to bank

Cash Book

The Master Rule — Learn This Once, Use Forever

When you START with Cash Book Balance (Favourable/Debit Balance):

Item

Do This

Cheque issued but NOT presented to bank

➕ ADD

Cheque deposited but NOT cleared by bank

➖ DEDUCT

Bank charges NOT in Cash Book

➖ DEDUCT

Interest/Dividend credited by bank NOT in Cash Book

➕ ADD

Direct deposit by customer NOT in Cash Book

➕ ADD

Direct payment by bank (insurance, EMI) NOT in Cash Book

➖ DEDUCT

Cheque deposited dishonoured (bounced) NOT in Cash Book

➖ DEDUCT

Cheque issued returned (technical reason) NOT in Cash Book

➕ ADD

Receipts side of Cash Book undercast

➕ ADD

Payments side of Cash Book undercast

➖ DEDUCT

Receipts side of Cash Book overcast

➖ DEDUCT

Payments side of Cash Book overcast

➕ ADD

Note: Result after applying all items = Pass Book Balance. If starting from Pass Book, FLIP every ADD and DEDUCT.

Overdraft — The Most Confusing Part (Explained Simply)

Normally your Cash Book shows a Debit Balance (money you have). When you spend more than you have, the bank gives you a temporary loan — now your Cash Book shows a Credit Balance. This is called Bank Overdraft (OD).

Situation

Normal Balance

Overdraft (OD)

Cheque issued not presented

➕ ADD

➖ DEDUCT

Cheque deposited not cleared

➖ DEDUCT

➕ ADD

Bank charges not in CB

➖ DEDUCT

➕ ADD

Interest by bank not in CB

➕ ADD

➖ DEDUCT

Level 1 — Basic BRS

QUESTION The Cash Book of Arun shows Dr. balance of ₹15,000 on 31st March 2024. On comparing with Pass Book, the following differences were found: (i) Cheques issued but not yet presented to bank — ₹4,000 (ii) Cheques deposited but not cleared — ₹3,000 (iii) Bank charges not entered in Cash Book — ₹250 (iv) Interest credited by bank not in Cash Book — ₹750 Prepare BRS and find Pass Book balance.

Bank Reconciliation Statement of Arun

As on 31st March 2024

Particulars

₹

₹

Balance as per Cash Book (Dr.)

15,000

ADD:

Cheques issued but not presented to bank

4,000

Interest credited by bank (not in Cash Book)

750

4,750

19,750

LESS:

Cheques deposited but not cleared by bank

3,000

Bank charges not in Cash Book

250

3,250

Balance as per Pass Book (Cr.)

16,500

Level 2 — Find Cash Book Balance (Working Backwards)

QUESTION Pass Book of Meena shows Cr. balance of ₹20,000 on 31st March 2024. (i) Cheques issued but not presented — ₹5,000 (ii) Cheques deposited but not cleared — ₹3,500 (iii) Bank paid LIC premium directly — ₹1,500 (iv) Dividend collected by bank — ₹2,000 (v) Bank charges — ₹300 Find Cash Book balance.

Understanding Casting Errors: Receipts side undercast → CB balance is LESS → ADD the short amount Receipts side overcast → CB balance is MORE → DEDUCT the excess Payments side undercast → CB balance is MORE → DEDUCT the short amount Payments side overcast → CB balance is LESS → ADD the excess

QUESTION Cash Book shows Dr. balance of ₹12,000 on 30th June 2024. (i) Cheques deposited ₹8,000 — only ₹6,500 credited by bank (ii) Receipts column of Cash Book undercast by ₹200 (iii) Customer deposited ₹3,000 directly in bank — only in Pass Book (iv) Cheques issued ₹9,200 — only ₹2,200 presented for payment in July (v) Bank credited interest ₹330; bank charges ₹60 Prepare BRS.

Key Workings Cheques issued not presented = Rs.9,200 – Rs.2,200 = Rs.7,000 Cheques deposited not cleared = Rs.8,000 – Rs.6,500 = Rs.1,500 Receipts undercast -> CB balance is less -> ADD Rs.200

Bank Reconciliation Statement

As on 30th June 2024

Particulars

₹

₹

Balance as per Cash Book (Dr.)

12,000

ADD:

Cheques issued but not presented (9,200 – 2,200)

7,000

CB receipts undercast (add short amount)

200

Customer direct deposit not in CB

3,000

Interest credited by bank

330

10,530

22,530

LESS:

Cheques deposited but not cleared (8,000 – 6,500)

1,500

Bank charges

60

1,560

Balance as per Pass Book (Cr.)

20,970

Level 4 — Wrong Amount Recorded

Golden Rule for Wrong Amount Errors: Adjustment = Correct amount – Wrong amount recorded (adjust only the DIFFERENCE, not full amount!)

QUESTION Cash Book (Dr. balance) ₹25,000 on 31st March 2024. (i) Cheques issued not presented — ₹6,000 (ii) Cheques deposited not cleared — ₹4,500 (iii) Bank charges not in CB — ₹300 (iv) Bank paid insurance ₹2,000 — recorded in CB as ₹200 (v) Interest by bank ₹800 — not in CB (vi) Cheque received ₹2,000 deposited — dishonoured, not in CB

Key Working — Item (iv) Wrong Amount Insurance actually paid = Rs.2,000 Recorded in Cash Book = Rs.200 CB shows Rs.1,800 MORE than it should -> DEDUCT Rs.1,800 (the difference only, NOT the full amount!)

Bank Reconciliation Statement

As on 31st March 2024

Particulars

₹

₹

Balance as per Cash Book (Dr.)

25,000

ADD:

Cheques issued but not presented

6,000

Interest credited by bank (not in CB)

800

6,800

31,800

LESS:

Cheques deposited but not cleared

4,500

Bank charges (not in CB)

300

Insurance short recorded (2,000 – 200)

1,800

Dishonoured cheque (not in CB)

2,000

8,600

Balance as per Pass Book (Cr.)

23,200

Level 5 — Bills of Exchange in BRS

Term

Meaning

Bill Discounted

You gave a bill to bank; bank gave money immediately at a small discount

Bill Retired

Bill paid before due date — bank gives you a rebate (discount for early payment)

Bill Dishonoured

Bill not paid on due date — bank reverses the payment and may charge extra

Bill for Collection

You gave bill to bank to collect on due date — bank credits when collected

QUESTION Cash Book shows Dr. balance of ₹10,000 on 31st December 2024. (i) Cheque to Karan ₹500 — not presented (ii) Bill ₹700 retired — rebate ₹20 — full ₹700 credited in Cash Book (iii) Cheque ₹295 deposited — dishonoured (iv) ₹800 deposited — credited in Pass Book as ₹80 (bank error) (v) Payments side CB undercast by ₹200 (vi) Bill receivable ₹1,000 discounted Nov — dishonoured 31st Dec — not in CB

Key Workings Item (ii): Bill retired. Rebate=20. CB shows 700 but bank credited 680. DEDUCT Rs.20 (rebate only) Item (iv): Bank error – credited 80 instead of 800. Bank credited 720 less. ADD Rs.720 Item (v): Payments undercast -> CB balance is MORE -> DEDUCT Rs.200

Bank Reconciliation Statement

As on 31st December 2024

Particulars

₹

₹

Balance as per Cash Book (Dr.)

10,000

ADD:

Cheque to Karan — not presented

500

Bank error — short credit (800 – 80)

720

1,220

11,220

LESS:

Rebate on bill not recorded in CB (700 – 680)

20

Cheque deposited — dishonoured

295

Payments side CB undercast

200

Bill discounted — dishonoured — not in CB

1,000

1,515

Balance as per Pass Book (Cr.)

9,705

Level 6 — Overdraft (OD) Question

QUESTION Cash Book shows Cr. balance (Overdraft) of ₹8,000 on 31st March 2024. (i) Cheques issued not presented — ₹2,000 (ii) Cheques deposited not cleared — ₹2,500 (iii) Interest on overdraft charged — ₹60 — not in CB (iv) Bank charges — ₹100 — not in CB (v) Pass Book shows credit ₹1,000 — ₹400 by debtor directly + ₹600 interest on investment — not in CB (vi) Cheque ₹200 recorded in CB but never sent to bank

Overdraft Rule — Everything FLIPS! Normal: Cheque issued not presented -> ADD | In OD: -> DEDUCT Normal: Cheque deposited not cleared -> DEDUCT | In OD: -> ADD Normal: Bank charges -> DEDUCT | In OD: -> ADD (increases what you owe)

Bank Reconciliation Statement

As on 31st March 2024

Particulars

₹

₹

Overdraft as per Cash Book (Cr.)

8,000

ADD: (Items that increase overdraft)

Cheques deposited but not cleared

2,500

Interest on OD not in CB

60

Bank charges not in CB

100

2,660

10,660

LESS: (Items that decrease overdraft)

Cheques issued but not presented

2,000

Direct deposit by debtor + interest on investment

1,000

Cheque recorded in CB but never sent to bank

200

3,200

Overdraft as per Pass Book (Dr.)

7,460

Level 7 — Partial Cheques

Key Rule: Only the UNPRESENTED portion causes the BRS difference. Cheques presented BEFORE the date = already in both books = NO difference. Ignore them.

QUESTION Cash Book (Dr. balance) ₹12,000 on 31st March 2024. (i) Total cheques issued ₹10,000 — ₹3,000 presented in March, ₹4,000 presented in April, rest not presented (ii) Total cheques deposited ₹5,000 — ₹1,500 credited in March, rest credited in April (iii) Bank charges ₹100; interest credited ₹200 (iv) CB receipts side undercast ₹500

Key Workings — Partial Cheques Cheques issued not yet presented = Rs.4,000 (April) + Rs.3,000 (never) = Rs.7,000 (Rs.3,000 presented in March = already in both books = no difference) Cheques deposited not cleared = Rs.5,000 – Rs.1,500 = Rs.3,500

QUESTION Starting from Pass Book Cr. balance ₹12,400 on 31st March 2024. (a) Cheques issued not presented ₹500 (b) Cheque issued returned on tech. grounds ₹4,000 — not in CB (c) Cheque deposited not in CB ₹500 (d) Commission charged ₹27; Interest allowed ₹330 (e) Amount wrongly debited by bank ₹2,400 (f) Short credit for cash deposit ₹90 (g) CB credit side undercast ₹200 (h) Insurance premium not in CB ₹600 (i) Bill for collection credited by bank ₹8,000 (j) Bank charges entered TWICE in CB ₹20 (k) Cheque received entered TWICE in CB ₹1,000 (l) Bill discounted dishonoured not in CB ₹5,000 (m) Rebate on payment of bill by bank not in CB ₹200

Bank Reconciliation Statement

As on 31st March 2024 | Starting from Pass Book Balance

Particulars

₹

₹

Balance as per Pass Book (Cr.)

12,400

PLUS ITEMS (to reach Cash Book):

(c) Cheque deposited not recorded in CB

500

(g) CB credit side undercast

200

(j) Bank charges entered twice in CB

20

(i) Bill for collection credited by bank

8,000

(m) Rebate on payment of bill not in CB

200

MINUS ITEMS (to reach Cash Book):

(a) Cheques issued not presented

500

(b) Cheque issued returned — not in CB

4,000

(d) Interest allowed by bank — not in CB

330

(d) Commission charged by bank

27

(e) Amount wrongly debited by bank (bank error)

2,400

(f) Short credit for cash deposit (bank error)

90

(h) Insurance premium not recorded in CB

600

(k) Cheque received entered twice in CB

1,000

(l) Bill discounted dishonoured — not in CB

5,000

Balance as per Cash Book (Dr.) = 12,400 + 8,920 – 13,947

7,373

Master Cheat Sheet — Every Item at a Glance

Item

Start from CB (Dr.)

Start from PB (Cr.)

Cheque issued not presented

➕ ADD

➖ DEDUCT

Cheque deposited not cleared

➖ DEDUCT

➕ ADD

Bank charges not in CB

➖ DEDUCT

➕ ADD

Interest credited by bank not in CB

➕ ADD

➖ DEDUCT

Direct deposit by customer not in CB

➕ ADD

➖ DEDUCT

Direct payment by bank not in CB

➖ DEDUCT

➕ ADD

Cheque dishonoured not in CB

➖ DEDUCT

➕ ADD

Cheque issued returned not in CB

➕ ADD

➖ DEDUCT

CB receipts undercast

➕ ADD

➖ DEDUCT

CB payments undercast

➖ DEDUCT

➕ ADD

CB receipts overcast

➖ DEDUCT

➕ ADD

CB payments overcast

➕ ADD

➖ DEDUCT

Bill discounted dishonoured not in CB

➖ DEDUCT

➕ ADD

Rebate on bill — full amount in CB

➖ rebate only

➕ rebate only

Bank error — excess debit

➕ ADD

➖ DEDUCT

Bank error — short credit

➕ ADD

➖ DEDUCT

5-Minute Exam Revision — Memory Tricks

1. Issued not presented → ADD (from CB) 2. Deposited not cleared → DEDUCT (from CB) 3. Bank does something without telling me → find the direction 4. Overdraft → flip every rule 5. Partial cheques → only unpresented portion counts 6. Wrong amount → adjust only the difference, not full amount 7. Casting error → think: does it make CB more or less?

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.