When you buy an asset like machinery, furniture, or a vehicle — it does not stay new forever. Every year its value reduces due to constant use, passage of time, obsolescence, or accidents.

Simple Definition Depreciation = The reduction in value of a fixed asset over time due to use, wear & tear, or obsolescence.

2. Why is Depreciation Charged?

Reason

Explanation

True Profit

Without depreciation, profit is overstated — misleading stakeholders

True Asset Value

Balance Sheet shows correct book value of assets

Replacement Fund

Helps save money to buy a new asset when the old one becomes useless

Matching Principle

Cost matched with revenue earned using that asset in the same period

Legal Requirement

Companies Act requires charging depreciation before declaring dividend

3. Key Terms — Understand These First

Term

Meaning

Example

Cost of Asset

Total purchase price + installation + freight charges

Machine ₹1,00,000 + freight ₹5,000 = ₹1,05,000

Scrap Value

Amount received when asset is sold at end of its useful life

₹5,000

Depreciable Cost

Cost − Scrap Value = Amount to be depreciated over useful life

₹1,05,000 − ₹5,000 = ₹1,00,000

Useful Life

How many years the asset will be productively used

10 years

Book Value / WDV

Cost − Total Depreciation charged so far (reduces every year)

₹80,000 after Year 2

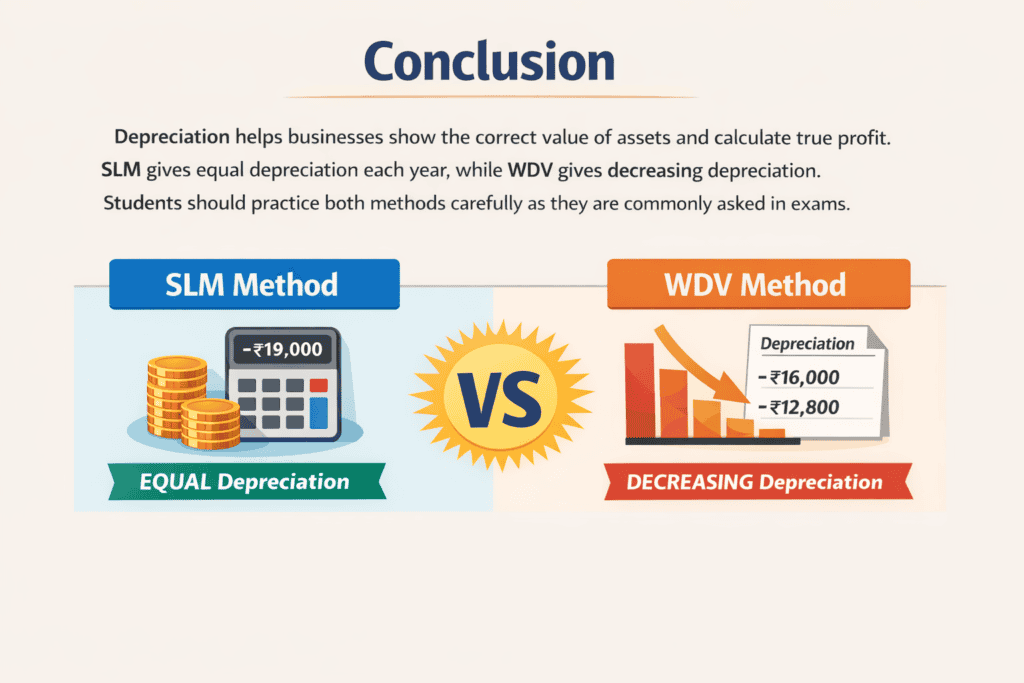

4. SLM vs WDV — Key Differences at a Glance

Feature

SLM (Straight Line Method)

WDV (Written Down Value)

Full Name

Straight Line Method

Written Down Value Method

Also Called

Fixed Instalment / Original Cost Method

Reducing Balance / Diminishing Balance Method

Depreciation Amount

Same every year (FIXED)

Reduces every year (DECREASING)

Calculated On

Original Cost of Asset

Book Value (reducing balance each year)

Book Value at End

Becomes exactly Scrap Value

Never becomes zero

Best Suited For

Furniture, patents, leases

Machinery, vehicles, computers

Recognised by

Income Tax Act

Companies Act (Schedule II)

5. Method 1 — Straight Line Method (SLM)

SLM Formula: Annual Depreciation = (Cost of Asset − Scrap Value) ÷ Useful Life Rate of Depreciation = (Annual Depreciation ÷ Cost of Asset) × 100

Level 1 — SLM Basic (3-Year Ledger)

QUESTION A machine is purchased on 1st April 2021 for ₹1,00,000. Installation charges ₹5,000. Estimated scrap value ₹10,000. Useful life 5 years. Books closed on 31st March every year. Prepare Machinery Account for 3 years under SLM.

Working — SLM Calculation Cost of Machine = ₹1,00,000 + ₹5,000 (installation) = ₹1,05,000 Scrap Value = ₹10,000 Depreciable Cost = ₹1,05,000 − ₹10,000 = ₹95,000 Annual Dep (SLM) = ₹95,000 ÷ 5 years = ₹19,000 per year (FIXED every year)

Dr. Machinery Account Cr.

Dr.

Cr.

Date

Particulars

Amount (₹)

Date

Particulars

Amount (₹)

Year 2021-22

Year 2021-22

Apr 1

Bank A/c

1,05,000

Mar 31

Depreciation A/c

19,000

Year 2022-23

Mar 31

Balance c/d

86,000

Apr 1

Balance b/d

86,000

Year 2022-23

Year 2023-24

Mar 31

Depreciation A/c

19,000

Apr 1

Balance b/d

67,000

Mar 31

Balance c/d

67,000

Year 2023-24

Mar 31

Depreciation A/c

19,000

Mar 31

Balance c/d

48,000

✅ Note: Depreciation is ₹19,000 every year — FIXED under SLM. Book Value reduces by equal amount each year.

6. Method 2 — Written Down Value Method (WDV)

WDV Formula: Annual Depreciation = Book Value at Beginning of Year × Rate ÷ 100 (Note: Book Value reduces every year, so Depreciation also reduces!)

Level 2 — WDV Basic (3-Year Ledger)

QUESTION A machine purchased on 1st April 2021 for ₹1,00,000. Depreciation charged at 20% p.a. under WDV method. Books closed 31st March. Prepare Machinery Account for 3 years.

Working — WDV Year-wise Calculation Year 1: ₹1,00,000 × 20% = ₹20,000 → Book Value = ₹80,000 Year 2: ₹80,000 × 20% = ₹16,000 → Book Value = ₹64,000 Year 3: ₹64,000 × 20% = ₹12,800 → Book Value = ₹51,200

Dr. Machinery Account Cr.

Dr.

Cr.

Date

Particulars

Amount (₹)

Date

Particulars

Amount (₹)

Year 2021-22

Year 2021-22

Apr 1

Bank A/c

1,00,000

Mar 31

Depreciation A/c

20,000

Year 2022-23

Mar 31

Balance c/d

80,000

Apr 1

Balance b/d

80,000

Year 2022-23

Year 2023-24

Mar 31

Depreciation A/c

16,000

Apr 1

Balance b/d

64,000

Mar 31

Balance c/d

64,000

Year 2023-24

Mar 31

Depreciation A/c

12,800

Mar 31

Balance c/d

51,200

✅ Note: Depreciation DECREASES every year under WDV → ₹20,000 → ₹16,000 → ₹12,800. This is the key difference from SLM!

QUESTION Machinery purchased on 1st July 2021 for ₹60,000. Depreciation @ 10% p.a. SLM. Books closed 31st March every year. Prepare Machinery Account for 2 years.

Working — Proportionate Months Year 1 (Jul 2021 → Mar 2022) = 9 months only Dep = ₹60,000 × 10% × 9/12 = ₹4,500 Year 2 (Apr 2022 → Mar 2023) = 12 months (full year) Dep = ₹60,000 × 10% = ₹6,000

Dr. Machinery Account Cr.

Dr.

Cr.

Date

Particulars

Amount (₹)

Date

Particulars

Amount (₹)

Year 2021-22

Year 2021-22 (9 months)

Jul 1

Bank A/c

60,000

Mar 31

Depreciation A/c (9 months)

4,500

Year 2022-23

Mar 31

Balance c/d

55,500

Apr 1

Balance b/d

55,500

Year 2022-23 (12 months)

Mar 31

Depreciation A/c (12 months)

6,000

Mar 31

Balance c/d

49,500

8. Level 4 — Addition of Asset During the Year

QUESTION On 1st April 2021, machinery purchased for ₹80,000. On 1st October 2021, additional machinery purchased for ₹40,000. Depreciation @ 10% p.a. SLM. Books closed 31st March. Prepare account for 2 years.

Working — Year-wise Depreciation Year 1 (2021-22): Old Machine = ₹80,000 × 10% × 12/12 = ₹8,000 New Machine = ₹40,000 × 10% × 6/12 = ₹2,000 (Oct to Mar = 6 months) Total Year 1 Depreciation = ₹10,000 Year 2 (2022-23): Old Machine = ₹80,000 × 10% = ₹8,000 New Machine = ₹40,000 × 10% = ₹4,000 Total Year 2 Depreciation = ₹12,000

Dr. Machinery Account Cr.

Dr.

Cr.

Date

Particulars

Amount (₹)

Date

Particulars

Amount (₹)

Year 2021-22

Year 2021-22

Apr 1

Bank A/c (Old Machine)

80,000

Mar 31

Depreciation A/c

10,000

Oct 1

Bank A/c (New Machine)

40,000

Mar 31

Balance c/d

1,10,000

Total

1,20,000

Total

1,20,000

Year 2022-23

Year 2022-23

Apr 1

Balance b/d

1,10,000

Mar 31

Depreciation A/c

12,000

Total

1,10,000

Mar 31

Balance c/d

98,000

Total

1,10,000

9. Level 5 — Sale of Asset (Profit or Loss on Sale)

Steps for Sale of Asset (Always follow this order): Step 1: Charge depreciation up to date of sale Step 2: Calculate Book Value on date of sale Step 3: Compare Sale Price vs Book Value Step 4: Difference = Profit (if SP > BV) or Loss (if SP < BV) Step 5: Transfer to Profit & Loss Account

QUESTION Machinery purchased on 1st April 2020 for ₹1,20,000. Depreciation @ 10% p.a. SLM. On 30th September 2022, machine sold for ₹85,000. Books closed 31st March. Show Machinery Account.

Working — Step by Step Annual Dep (SLM) = ₹1,20,000 × 10% = ₹12,000 Year 1 (2020-21): Dep = ₹12,000 → BV = ₹1,08,000 Year 2 (2021-22): Dep = ₹12,000 → BV = ₹96,000 Year 3 (Apr–Sep 2022 = 6 months): Dep = ₹12,000 × 6/12 = ₹6,000 Book Value on sale date = ₹96,000 − ₹6,000 = ₹90,000 Sale Price = ₹85,000 | Book Value = ₹90,000 LOSS ON SALE = ₹90,000 − ₹85,000 = ₹5,000

Dr. Machinery Account Cr.

Dr.

Cr.

Date

Particulars

Amount (₹)

Date

Particulars

Amount (₹)

Year 2020-21

Year 2020-21

Apr 1

Bank A/c

1,20,000

Mar 31

Depreciation A/c

12,000

Year 2021-22

Mar 31

Balance c/d

1,08,000

Apr 1

Balance b/d

1,08,000

Year 2021-22

Year 2022-23

Mar 31

Depreciation A/c

12,000

Apr 1

Balance b/d

96,000

Mar 31

Balance c/d

96,000

Year 2022-23 (Sold — 6 months)

Sep 30

Depreciation A/c (6 months)

6,000

Sep 30

Bank A/c (Sale Proceeds)

85,000

Sep 30

Loss on Sale (P&L A/c)

5,000

✅ Note: Loss on Sale = Book Value (₹90,000) − Sale Price (₹85,000) = ₹5,000. Transferred to Profit & Loss Account.

10. Level 6 — Change of Method: SLM to WDV (Retrospective)

⚠️ This is the HARDEST question type — 90% of students fail this! Master it here. Step 1: Find depreciation already charged under OLD method (total) Step 2: Find depreciation that SHOULD have been charged under NEW method Step 3: Difference = Short Charged or Excess Charged Step 4: Adjust in current year P&L Account Step 5: New book value = WDV book value going forward

QUESTION Machine purchased on 1st April 2020 for ₹2,00,000. Scrap value ₹20,000. Life 9 years. Depreciation charged under SLM for 3 years. From 1st April 2023, company decides to change to WDV @ 20% p.a. with retrospective effect. Show the adjustment entry and Machinery Account for year 2023-24.

Step 1 — SLM Already Charged (3 Years) Annual SLM = (₹2,00,000 − ₹20,000) ÷ 9 = ₹20,000 per year 3 Years SLM Depreciation = ₹20,000 × 3 = ₹60,000 Book Value as per SLM after 3 years = ₹2,00,000 − ₹60,000 = ₹1,40,000

Step 2 — WDV That SHOULD Have Been Charged (3 Years) Year 1: ₹2,00,000 × 20% = ₹40,000 → BV = ₹1,60,000 Year 2: ₹1,60,000 × 20% = ₹32,000 → BV = ₹1,28,000 Year 3: ₹1,28,000 × 20% = ₹25,600 → BV = ₹1,02,400 Total WDV for 3 years = ₹97,600

Step 3 & 4 — Difference and Adjustment WDV Depreciation (should have been) = ₹97,600 SLM Depreciation (already charged) = ₹60,000 Short Charged = ₹37,600 → Debit Profit & Loss A/c Adjustment Entry: Profit & Loss A/c Dr. ₹37,600 | To Machinery A/c ₹37,600 New Book Value from 1st April 2023 = ₹1,02,400 (WDV after 3 years) Year 4 Depreciation (WDV) = ₹1,02,400 × 20% = ₹20,480

Dr. Machinery Account (Year 2023-24) Cr.

Dr.

Cr.

Date

Particulars

Amount (₹)

Date

Particulars

Amount (₹)

Year 2023-24

Year 2023-24

Apr 1

Balance b/d (SLM BV)

1,40,000

Apr 1

P&L A/c (Adjustment)

37,600

Total

1,40,000

Mar 31

Depreciation A/c (WDV)

20,480

Mar 31

Balance c/d

81,920

Total

1,40,000

11. Level 7 — Find Rate of Depreciation (Reverse Calculation)

QUESTION A machine was purchased for ₹1,00,000 on 1st April 2020. After 3 years the book value is ₹51,200 under WDV method. Find the rate of depreciation.

Working — Reverse WDV Formula Under WDV after n years: BV = Cost × (1 − r/100)ⁿ 51,200 = 1,00,000 × (1 − r/100)³ (1 − r/100)³ = 51,200 ÷ 1,00,000 = 0.512 (1 − r/100) = Cube Root of 0.512 = 0.8 r/100 = 1 − 0.8 = 0.2 Rate = 0.2 × 100 = 20% p.a.

Verification — Confirm the Answer Year 1: ₹1,00,000 × 20% = ₹20,000 → BV = ₹80,000 Year 2: ₹80,000 × 20% = ₹16,000 → BV = ₹64,000 Year 3: ₹64,000 × 20% = ₹12,800 → BV = ₹51,200 ✅ CORRECT!

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.