After recording all business transactions in the Journal and posting them into Ledger Accounts, the next step is preparing a Trial Balance.

A Trial Balance is a statement prepared on a particular date to check whether the total debit balances and total credit balances of all ledger accounts are equal.

If the total of the debit side is equal to the total of the credit side, the books are considered arithmetically correct.

Purpose of Trial Balance

To check the arithmetical accuracy of accounts

To summarize all ledger balances in one place

To help in preparing Final Accounts

To locate accounting mistakes

To prepare Trading Account, Profit and Loss Account and Balance Sheet

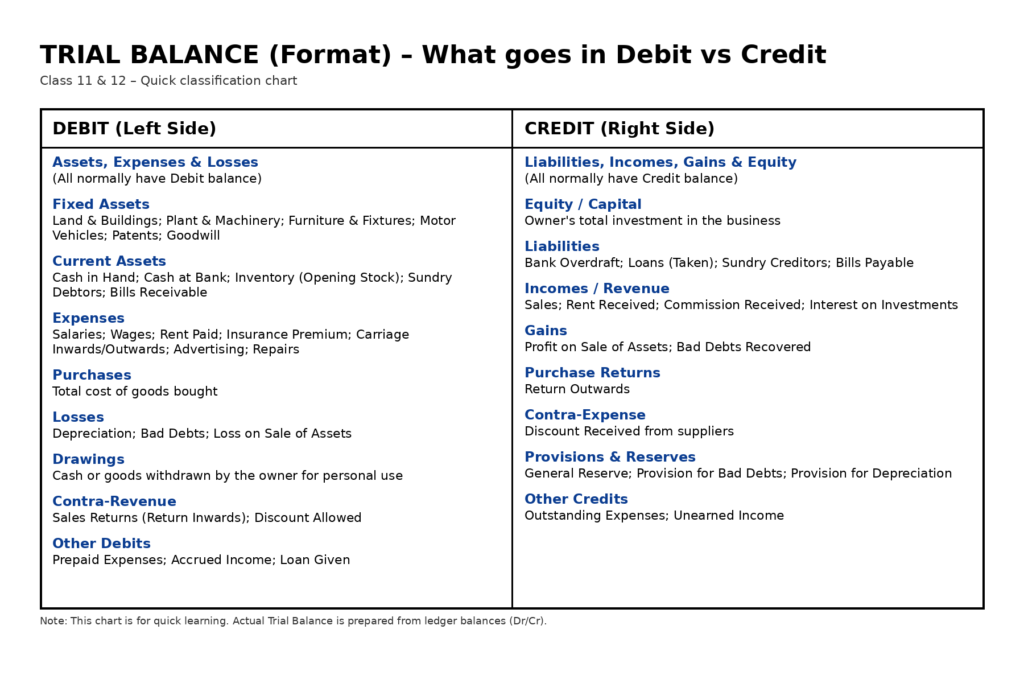

DEAD CLIC Rule

This is an easy memory trick to identify which accounts come under Debit and Credit.

Side

Letter

Meaning

Debit

D

Drawings

Debit

E

Expenses and Losses

Debit

A

Assets

Debit

D

Discount Allowed

Credit

C

Capital

Credit

L

Liabilities

Credit

I

Income and Gains

Credit

C

Creditors / Sales

Problem 1: Basic Fundamentals

Question Data

Account Name

Amount (₹)

Cash

50,000

Capital

2,00,000

Purchases

80,000

Sales

1,20,000

Salary

30,000

Rent

15,000

Debtors

75,000

Creditors

40,000

Furniture

1,10,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Cash

50,000

2

Purchases

80,000

3

Salary

30,000

4

Rent

15,000

5

Debtors

75,000

6

Furniture

1,10,000

7

Capital

2,00,000

8

Sales

1,20,000

9

Creditors

40,000

Total

3,60,000

3,60,000

Problem 2: Returns and Discounts

Question Data

Account Name

Amount (₹)

Opening Stock

25,000

Purchases

1,50,000

Sales

2,00,000

Returns Inward

10,000

Returns Outward

8,000

Wages

20,000

Discount Allowed

3,000

Capital

1,50,000

Building

67,000

Creditors

35,000

Bank Balance

60,000

Discount Received

2,000

Debtors

55,000

Carriage Inward

5,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Opening Stock

25,000

2

Purchases

1,50,000

3

Returns Inward

10,000

4

Wages

20,000

5

Discount Allowed

3,000

6

Building

67,000

7

Bank Balance

60,000

8

Debtors

55,000

9

Carriage Inward

5,000

10

Sales

2,00,000

11

Returns Outward

8,000

12

Discount Received

2,000

13

Capital

1,50,000

14

Creditors

35,000

Total

3,95,000

3,95,000

Problem 3: Closing Stock Adjustment

Note: Closing Stock = ₹30,000. Closing Stock does not appear in the Trial Balance.

Question Data

Account Name

Amount (₹)

Cash in Hand

15,000

Cash at Bank

45,000

Capital

3,00,000

Opening Stock

40,000

Drawings

20,000

Purchases

2,00,000

Sales

2,80,000

Expenses

85,000

Debtors

80,000

Creditors

55,000

Machinery

1,50,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Cash in Hand

15,000

2

Cash at Bank

45,000

3

Drawings

20,000

4

Opening Stock

40,000

5

Purchases

2,00,000

6

Expenses

85,000

7

Debtors

80,000

8

Machinery

1,50,000

9

Capital

3,00,000

10

Sales

2,80,000

11

Creditors

55,000

Total

6,35,000

6,35,000

Problem 4: High Capital Scenario

Question Data

Account Name

Amount (₹)

Capital

5,00,000

Cash

1,00,000

Bank

2,00,000

Purchases

1,50,000

Sales

2,00,000

Debtors

80,000

Salary

20,000

Rent

10,000

Creditors

60,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Cash

1,00,000

2

Bank

2,00,000

3

Debtors

80,000

4

Purchases

1,50,000

5

Salary

20,000

6

Rent

10,000

7

Capital

5,00,000

8

Sales

2,00,000

9

Creditors

60,000

Total

5,60,000

5,60,000

Problem 5: Manufacturing Business

Question Data

Account Name

Amount (₹)

Machinery

3,00,000

Capital

4,00,000

Purchases

1,20,000

Sales

1,80,000

Wages

40,000

Debtors

70,000

Creditors

50,000

Cash

1,00,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Machinery

3,00,000

2

Purchases

1,20,000

3

Wages

40,000

4

Debtors

70,000

5

Cash

1,00,000

6

Capital

4,00,000

7

Sales

1,80,000

8

Creditors

50,000

Total

6,30,000

6,30,000

Problem 6: Service Business

Question Data

Account Name

Amount (₹)

Professional Fees

90,000

Computer

45,000

Drawings

5,000

Cash

75,000

Office Rent

12,000

Electricity

3,000

Capital

50,000

Creditors

10,000

Prepaid Rent

10,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Computer

45,000

2

Cash

75,000

3

Prepaid Rent

10,000

4

Drawings

5,000

5

Office Rent

12,000

6

Electricity

3,000

7

Professional Fees

90,000

8

Capital

50,000

9

Creditors

10,000

Total

1,50,000

1,50,000

Problem 7: Small Business

Question Data

Account Name

Amount (₹)

Opening Stock

10,000

Purchases

35,000

Debtors

18,000

Stationery

2,000

Sales

60,000

Creditors

12,000

Capital

40,000

Furniture

47,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Opening Stock

10,000

2

Purchases

35,000

3

Debtors

18,000

4

Stationery

2,000

5

Furniture

47,000

6

Sales

60,000

7

Creditors

12,000

8

Capital

40,000

Total

1,12,000

1,12,000

Problem 8: Reserves and Provisions

Question Data

Account Name

Amount (₹)

Machinery

2,00,000

Capital

2,50,000

Debtors

1,00,000

Purchases

2,20,000

Sales

3,00,000

Bad Debts

5,000

Provision for Bad Debts

2,000

Creditors

70,000

Bank Overdraft

3,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Machinery

2,00,000

2

Debtors

1,00,000

3

Purchases

2,20,000

4

Bad Debts

5,000

5

Capital

2,50,000

6

Sales

3,00,000

7

Provision for Bad Debts

2,000

8

Creditors

70,000

9

Bank Overdraft

3,000

Total

5,25,000

5,25,000

Problem 9: Transport Business

Question Data

Account Name

Amount (₹)

Vehicles

8,00,000

Service Revenue

4,00,000

Capital

2,00,000

Cash at Bank

2,10,000

Fuel and Oil

50,000

Loan from Bank

5,00,000

Interest on Loan

40,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Vehicles

8,00,000

2

Fuel and Oil

50,000

3

Cash at Bank

2,10,000

4

Interest on Loan

40,000

5

Service Revenue

4,00,000

6

Loan from Bank

5,00,000

7

Capital

2,00,000

Total

11,00,000

11,00,000

Problem 10: General Store

Question Data

Account Name

Amount (₹)

Opening Stock

15,000

Purchases

60,000

Furniture

20,000

Debtors

25,000

Cash

33,000

Sales

95,000

Creditors

10,000

Capital

50,000

Carriage Outward

2,000

Solution

S.No

Account Name

Debit (₹)

Credit (₹)

1

Opening Stock

15,000

2

Purchases

60,000

3

Furniture

20,000

4

Debtors

25,000

5

Cash

33,000

6

Carriage Outward

2,000

7

Sales

95,000

8

Creditors

10,000

9

Capital

50,000

Total

1,55,000

1,55,000

Important Rules to Remember

Assets always come on the Debit side.

Expenses and losses always come on the Debit side.

Capital always comes on the Credit side.

Liabilities always come on the Credit side.

Income and gains always come on the Credit side.

Drawings always come on the Debit side.

Closing stock usually does not appear in the Trial Balance.

Swathika B is an MBA graduate in Finance & Business Analytics , the founder of The Commerce Lab. With a strong academic foundation in B.Com BFSI and hands-on experience in financial analysis, data analytics, and business studies, she created this platform to make Commerce and Accountancy simple, practical, and exam-ready for students across India.